Why Saving in Your 60s Still Matters More Than You Think

Entering your 60s doesn’t mean the “saving” chapter is closed; it just means the rules of the game change. You’re closer to retirement, true, but you also have more clarity: your kids might be independent, your mortgage could be smaller, and your income is usually higher than in your 40s or 50s. This is exactly why retirement planning in your 60s can be extremely effective, if you approach it deliberately instead of emotionally. The goal now is not to chase risky growth, but to close any gaps, reduce big financial threats, and turn your savings into a reliable income stream you can actually live on without constant money worries.

—

Key Terms You’ll Hear (In Plain English)

Core Retirement Definitions You Need

Before talking about how to save for a comfortable retirement in your 60s, it helps to decode the jargon you’ll run into. Let’s keep it simple and practical:

– Retirement nest egg – the total amount of money and assets you’ve set aside for retirement. This includes pensions, 401(k)/IRA balances, brokerage accounts, cash, sometimes rental property equity.

– Withdrawal rate – the percentage of your retirement savings you take out each year to live on. For example, if you have $500,000 and withdraw $20,000 a year, that’s a 4% withdrawal rate.

– Retirement income – the money that will hit your bank account after you stop working: Social Security, pensions, annuity payments, investment withdrawals, rental income, maybe part-time work.

– Longevity risk – the risk of outliving your money. It’s not just about how much you have at 65, but whether it can last into your 80s or 90s.

– Sequence-of-returns risk – the danger that bad market years happen early in retirement. If markets drop right when you start withdrawing, you may be forced to sell at low prices, hurting your long-term balance.

– Inflation risk – the risk that prices for food, housing, and healthcare rise faster than your income, slowly eroding your purchasing power.

These definitions matter because every decision you make in your 60s—what to invest in, when to retire, how much to spend—affects one or more of these risks. The practical side of retirement planning in your 60s is learning to nudge each of these in your favor.

—

Step 1: Get a Clear, Honest Picture of Where You Stand

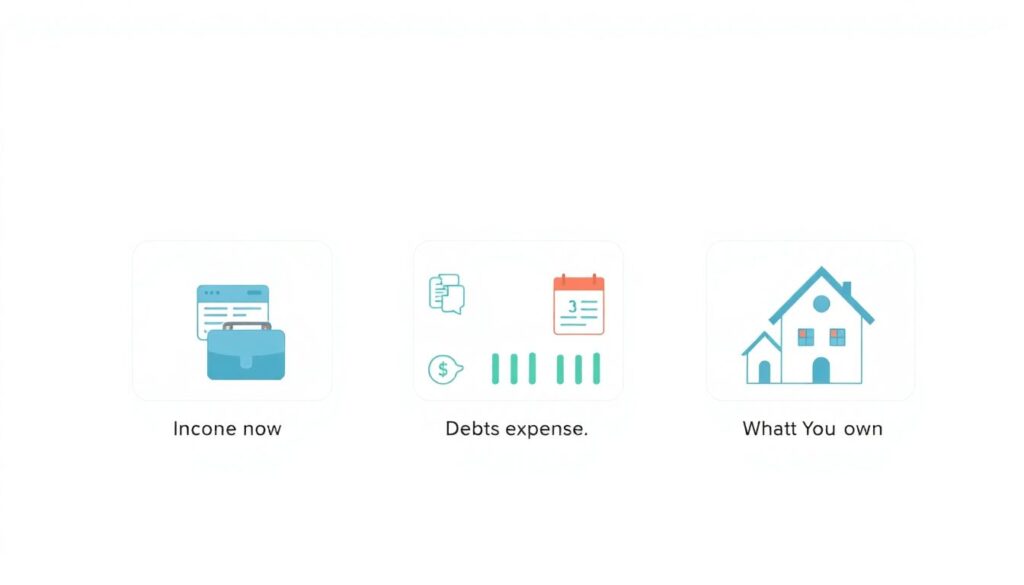

Build a Simple “Retirement Dashboard”

Think of your finances as a dashboard instead of a messy stack of statements. You want to see, at a glance, what’s coming in, what you owe, and what you own.

Diagram (text version):

Imagine three boxes in a row:

– Box 1: “Income Now” → salary, business income, side gigs

– Box 2: “Debts & Expenses” → mortgage, car loans, living costs

– Box 3: “Assets & Savings” → 401(k)/IRA, brokerage, cash, home equity

An arrow moves from Box 1 (Income Now) to Box 3 (Assets & Savings), and a separate arrow moves from Box 1 to Box 2 (Debts & Expenses). Your job in your 60s is to thicken the arrow from income to savings and thin the arrow from income to debts, without ignoring your real-life lifestyle.

Practical Checklist: What to Gather

Pull together:

– Current balances for all retirement accounts (401(k), 403(b), IRAs, etc.)

– Brokerage and bank account balances

– Pension estimates and Social Security statements

– Mortgage, car loans, credit cards, personal loans (with interest rates)

– Monthly spending breakdown (even a rough one is better than nothing)

When you see everything on one page, it becomes much easier to see how to catch up on retirement savings in your 60s because you can spot obvious leaks (like high-interest debt) and underused resources (like free employer matches).

—

Step 2: Define “Comfortable” Instead of “Perfect”

Translate Lifestyle into Monthly Numbers

“Comfortable retirement” is vague until you express it in numbers. You don’t need a perfect forecast, just a reasonable ballpark. Ask yourself:

– Where do I want to live (current city, cheaper area, with family)?

– How often do I realistically plan to travel?

– What level of help might I need later (home care, assisted living, none)?

– What won’t I spend on anymore (commuting, work clothes, lunches out)?

Now convert this to monthly target spending. For example:

– Essential costs (housing, food, utilities, insurance, medications)

– Nice-to-have costs (travel, hobbies, gifts, dining out)

– One-off or irregular costs (car replacement every X years, big trips)

If your target is, say, $4,000/month after tax, and you expect $2,000 from Social Security and $500 from a pension, then your savings need to cover about $1,500/month. That number is much less scary and more actionable than a giant lump sum you see in generic calculators.

Rule-of-Thumb vs. Custom Calculation

Many general rules say you need around 70–80% of your pre-retirement income as retirement income. That can be a helpful starting point, but if your mortgage is almost gone and your kids are independent, you might need less. On the flip side, if you want to travel aggressively for the first 10 years, you might need more early on. A custom approach keeps you from over-saving in panic or under-saving in denial.

—

Step 3: Catching Up in Your 60s Without Panicking

How to Catch Up on Retirement Savings in Your 60s

If you feel behind, you’re not alone. The key is to move from vague worry to specific action steps. In your 60s, the levers you still control are:

– Retirement age (work a bit longer or part-time)

– Savings rate (divert more of current income to savings)

– Spending level (trim recurring costs)

– Investment mix (more efficient, not necessarily more aggressive)

Practical moves that often have the biggest impact:

– Use catch-up contributions to 401(k)s and IRAs if allowed in your country/plan. In the U.S., people 50+ can contribute more than younger workers.

– Redirect any windfalls—bonuses, inheritance, home sale profits—straight into retirement rather than lifestyle upgrades.

– Accelerate paying down high-interest debt; every dollar not going to interest is a dollar that can grow for you.

Instead of obsessing over a “magic number,” focus on closing the gap between expected retirement income and desired spending, one piece at a time.

—

Step 4: Rethinking Debt and Big Expenses

Debt Strategy in Your 60s

High-interest debt in your 60s is like dragging a heavy anchor while trying to swim to shore. Clearing it is often more powerful than hunting for a higher investment return.

If you have:

– Credit cards or personal loans with high interest: prioritizing these can generate a “guaranteed return” equal to the interest rate you stop paying.

– Mortgage: the decision is more nuanced. Paying it off reduces monthly required expenses, but don’t drain all your liquid savings just to be mortgage-free if it leaves you cash-poor and vulnerable to emergencies.

In practical terms, many people in their 60s benefit from a “hybrid” approach: pay down expensive debt aggressively while still contributing enough to retirement accounts to capture any employer match and keep money growing tax-efficiently.

Comparing Approaches: Aggressive Paydown vs. Balanced Saving

– Aggressive paydown – feels emotionally satisfying (“debt-free!”) but can leave you with less invested for growth, and sometimes less flexibility.

– Balanced approach – some money goes to debt, some to savings. Often more effective overall, especially when interest rates on your debt are moderate and potential long-term investment returns are higher.

Use your expected retirement date as a guiding line: aim to have no toxic, high-interest debt by then, and ideally a much lighter fixed monthly bill load.

—

Step 5: Choosing Investments in Your 60s

What “Best Retirement Investment Options for Seniors” Really Means

When people search for the best retirement investment options for seniors, what they often want is “How do I not blow this?” In your 60s, the focus shifts from pure growth to a balance of:

– Enough growth to outpace inflation and last for decades

– Enough stability that a bad year won’t derail your retirement

– Enough liquidity so you can access funds without painful penalties

Typical building blocks (general, not personal advice):

– Broad stock funds or ETFs – for growth, but usually not as large a share as in your 30s or 40s.

– Bond funds or high-quality individual bonds – to provide stability and income.

– Cash or very short-term instruments – for near-term spending and an emergency buffer.

– Possibly annuities – in some cases, an immediate or deferred income annuity can convert part of your lump sum into guaranteed income; useful for longevity risk, but fees and terms matter.

Simple Mental Diagram: Buckets Strategy

Visualize three “buckets”:

1. Short-term bucket (0–3 years)

– Cash, money market, short-term bonds

– Used for everyday withdrawals and emergencies.

2. Medium-term bucket (3–10 years)

– Bonds, conservative balanced funds

– Refilled from the long-term bucket during good market periods.

3. Long-term bucket (10+ years)

– Stock-heavy funds, growth assets

– Left untouched for as long as possible so it can recover from market swings.

In practice, this “buckets” approach helps many people stay calm in downturns because they can see that their near-term cash needs are already covered.

—

Step 6: Deciding When and How to Retire

Full Stop vs. Gradual Exit

Retirement doesn’t have to be a light switch; it can be a dimmer. Instead of quitting work all at once at 65, many people now:

– Move to part-time or consulting roles

– Change to a less stressful job with lower pay

– Take seasonal or gig work to keep some income coming in

This “soft landing” has major financial benefits:

– You delay withdrawals from savings

– You may delay Social Security or other benefits, increasing future monthly amounts

– You keep some structure and social contact, which often improves quality of life

Comparing Two Scenarios

– Scenario A: Full retirement at 65, no work income

You need your savings to cover all of your spending gaps immediately. The withdrawal rate may be higher earlier, increasing risk.

– Scenario B: Partial retirement from 65–70 with reduced work income

Your savings can grow for a few more years, your withdrawal rate stays lower, and Social Security or pension benefits may increase due to delayed claiming.

Even a modest part-time income can dramatically improve the math of your retirement plan and give you more confidence about your future.

—

Step 7: Turning Savings into a Paycheck

From Pile of Money to Monthly Income

Saving is only half the story. The other half is retirement income planning services—in other words, the strategies and tools that turn your lump sums into a predictable cash flow. Think of this as “building your own pension.”

Common income approaches:

– Fixed percentage withdrawals – e.g., withdraw 3–4% of portfolio per year, adjusted as needed for market conditions.

– Time-based withdrawals – draw more in early “go-go years” (travel, hobbies) and intentionally lower spending in later years.

– Guaranteed income layer – combine Social Security, pension, and possibly some annuity to create a base income, then supplement from investments.

The art is matching your income pattern to your real life: more for travel in your 60s and 70s, more for healthcare later, with guardrails so you don’t overspend early and regret it later.

—

Step 8: Taxes, Social Security, and Other Technical Pieces

Why Tax Planning Still Matters in Your 60s

Tax rules can amplify or shrink your after-tax income. A few examples of why this matters:

– Which account you withdraw from first (tax-deferred, tax-free, taxable) can affect how long your money lasts.

– Social Security timing – claiming early gives you money sooner, but less per month for life; delaying increases benefits, especially important if you expect a long lifespan.

– Required minimum distributions (RMDs) – in some countries, you’ll be forced to withdraw from certain accounts after a specific age, whether you need the money or not.

Getting even a basic tax-aware strategy can add years to the life of your portfolio, especially if your nest egg is substantial.

—

Step 9: When and How to Seek Professional Help

Using a Financial Advisor Effectively

If you feel stuck trying to figure out priorities—whether to pay down debt, how to invest, when to claim benefits—it may be worth looking for a financial advisor for retirement planning near me rather than trying to learn everything from scratch.

What a good advisor can help with:

– Modeling retirement age options (65 vs 67 vs 70, etc.)

– Designing investments that fit your specific risk tolerance and income needs

– Building a tax-aware withdrawal strategy and Social Security timing

– Stress-testing your plan against market drops and long life expectancy

Be selective and ask how they get paid, what their fiduciary duty is, and what specific experience they have with people in their 60s, not just younger accumulators. An advisor is a tool, not a boss; you’re hiring someone to help you make better-informed decisions, not surrender control.

—

Step 10: Concrete Actions You Can Take This Year

Short List of Practical Moves

To keep this from staying theoretical, here are realistic, hands-on steps that fit most people in their 60s:

– Increase contributions to retirement accounts to the maximum allowed, especially catch-up amounts if they apply to you.

– Use any raises, bonuses, or debt payoffs as triggers to immediately bump up your monthly saving rate rather than raising your spending.

– Review your investment mix so you’re not unintentionally taking either extreme: overly risky (all stocks) or overly conservative (all cash).

– Create or adjust your emergency fund so you’re not forced to raid retirement accounts when a car breaks down or a medical bill appears.

– Run at least one basic retirement income projection (online calculator, advisor, or DIY spreadsheet) to see if your current path supports your target lifestyle.

—

Bullet-Point Recap: Guiding Principles in Your 60s

– You’re not too late: you still control when you retire, how much you spend, and how you invest.

– Comfortable retirement is a cash-flow question, not a bragging-rights net worth competition.

– Debt decisions, especially high-interest debt, can matter as much as investment returns.

– A flexible retirement age and part-time work can dramatically improve your numbers.

– Professional help is a tool; use it where it adds clarity, especially on taxes and withdrawals.

—

Final Thoughts: Calm, Not Chaos

Saving for a comfortable retirement in your 60s is less about heroic risk-taking and more about steady, well-prioritized moves. You define what “comfortable” looks like, build a clear picture of your current position, then adjust the levers you still have: work, saving, spending, and investment choices. With a practical plan, retirement planning in your 60s becomes less about fear of running out and more about designing a life you recognize and actually want to live—one that your money can realistically support.