Why Your Money Strategy Must Age With You

Money habits that work at 23 often backfire at 53. Income, risk tolerance, family load and health risks all shift, so trying to use one static blueprint is a recipe for financial drag. Modern experts recommend structuring financial planning by age 20s 30s 40s 50s as a lifecycle process: accumulation, optimization, risk‑management and decumulation. Think of each decade as a different “system configuration”: you tune savings rate, asset allocation, insurance coverage and debt levels to match that phase. Below is a practical, jargon‑light roadmap on how to manage money at different ages 20s 30s 40s 50s with concrete actions, not vague slogans.

Core Principles That Don’t Change With Age

Before splitting by decade, you need a few universal protocols. Every CFP I’ve worked with repeats the same three: maintain a positive savings rate, avoid expensive consumer debt and protect against catastrophic risks. In more technical terms, you’re managing cash‑flow surplus, cost of capital and downside risk. These fundamentals are invariant whether you’re 25 or 55. Layer on simple automation—auto‑transfer to savings and investments, auto‑pay on key bills—and you remove “willpower” from the system. The result is a baseline structure that each decade’s tweaks can build on, rather than reinventing everything from zero.

Your 20s: Build the Financial Operating System

Stabilize Cash Flow and Kill Bad Debt

In your 20s, income is volatile and lifestyle temptation is high, so the first objective is cash‑flow control. Create a lean but realistic budget that explicitly caps fixed costs like rent and car payments at a safe percentage of take‑home pay. Experts usually target total housing plus transport under 45% of net income to leave room for saving and investing. Prioritize wiping out high‑interest credit card balances because their annualized cost often exceeds any realistic investment return. Use simple tools—one main checking account, one savings account and a single tracking app—to see money in and out without friction.

- Set a fixed “pay yourself first” transfer the day your salary hits.

- Use 0% balance transfers only with a written payoff plan.

- Cap discretionary categories (eating out, subscriptions) in advance.

Launch Long-Term Investing Early

Compounding is the main edge in your 20s; you have time to recover from volatility, so risk capacity is high. Most fiduciary advisors recommend low‑cost, diversified index funds, tilted towards equities, as the best investment strategies in your 20s 30s 40s and 50s, but with the highest equity share right now. Aim for at least 15–20% of gross income into retirement vehicles if possible. If your employer offers a match, treat it as mandatory free money. Don’t chase “hot” assets. Instead, automate monthly contributions into a global stock index fund plus a small bond slice to learn how you react during market drawdowns.

- Contribute enough to get full employer match.

- Open a low‑fee brokerage if no workplace plan exists.

- Schedule an annual “allocation checkup” on your birthday.

Insurance and Skill Investing

In risk‑management terms, you are your largest asset in your 20s; your future earning power is worth more than your current portfolio. That’s why experts push for basic health insurance plus disability cover even before you obsess about exotic investments. A single accident can destroy your balance sheet. Parallel to this, allocate a defined “human capital budget” each year to skills that increase your lifetime earnings: certifications, technical courses, languages. Track return on investment by comparing cost with salary bumps or promotion speed. This mindset converts vague “self‑improvement” into measurable financial engineering.

Your 30s: Optimize, Protect and Scale

Upgrade Budgeting to Full Financial Architecture

By your 30s, life complexity explodes: partners, kids, mortgages, business ideas. Instead of a simple budget, think in terms of a household balance sheet and income statement. Inventory all assets, liabilities and recurring obligations yearly. This is where structured financial planning by age 20s 30s 40s 50s becomes more granular—cash reserves should equal three to six months of core expenses, and any toxic debt must be on a clear amortization schedule. Direct raises and bonuses primarily to assets, not lifestyle creep. Experts suggest using “incremental allocation rules”: e.g., 50% of every raise to investing, 30% to debt reduction, 20% to lifestyle upgrades.

- Maintain a dedicated emergency fund in a high‑yield savings account.

- Consolidate scattered small accounts to simplify oversight.

- Audit subscriptions and recurring charges twice a year.

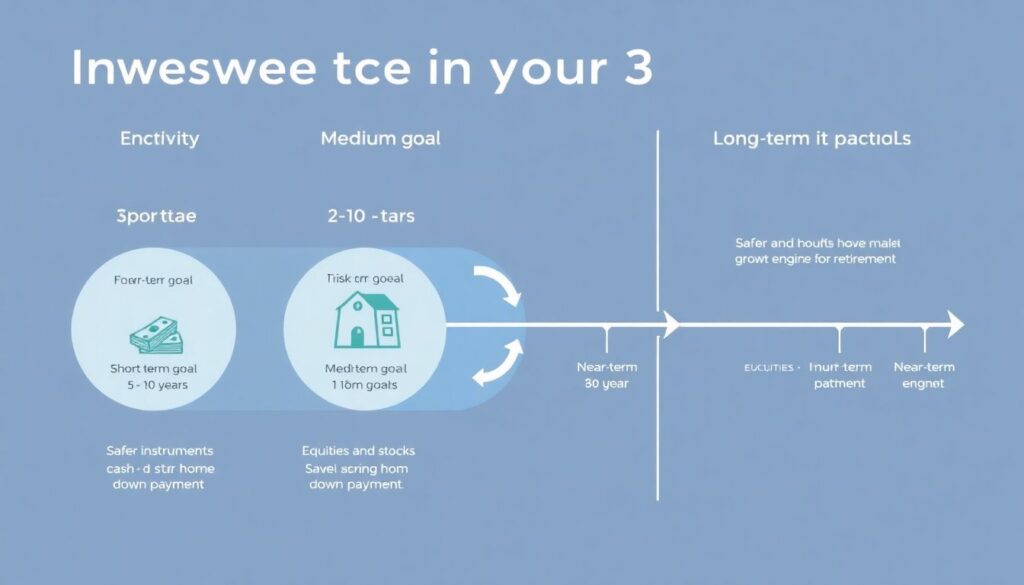

Align Investments With Concrete Time Horizons

Investment strategy in your 30s must reflect multiple time buckets: short‑term goals (3–5 years), medium‑term (5–10) and long‑term retirement. Use safer instruments (cash, short‑term bonds) for near‑term goals like a home down payment and keep equities for long‑range objectives. A typical expert allocation might still be equity‑heavy, but a bit less aggressive than in your 20s. Rebalancing annually keeps your risk profile stable as markets move. Treat any individual stock or crypto picks as a capped “sandbox” portion—perhaps 5–10% of your portfolio—so speculative choices don’t derail long‑term compounding if they implode.

Family, Housing and Risk Management

If you have dependents, risk management becomes non‑negotiable. Term life insurance covering 10–15 years of income is usually more cost‑effective than investment‑linked policies. For housing, calculate ownership versus renting using total cost of ownership: interest, property tax, maintenance and opportunity cost of your down payment. Experts warn against over‑leveraging into a property so large it starves your investment contributions. The financial stress of being “house poor” is a common failure mode in this decade. Integrate wills and basic estate documents now; it’s less about net worth size and more about legal clarity for children and partners.

Your 40s: Efficiency and Risk Balancing

Midlife Portfolio Audit and Catch-Up

At 40‑plus, your earnings are often near peak, but time to retirement shrinks. This is where personal finance advice for every age 20s 30s 40s 50s converges on aggressive but controlled saving rates. Calculate your projected retirement number using conservative assumptions: modest real returns, realistic spending and longevity into your 90s. If you’re behind, use catch‑up contributions where available and push savings rates into the 20–30% of gross income range if feasible. A midlife portfolio audit with a fee‑only planner can uncover tax inefficiencies, concentration risks and hidden fee drag that quietly erode your future spending power.

- Shift gradually towards a more balanced stock/bond mix.

- Reduce exposure to single‑stock or employer‑stock risk.

- Tax‑loss harvest in taxable accounts when markets dip.

Debt De-Risking and Lifestyle Calibration

Your 40s are a strategic window for liability reduction. Aim to eliminate non‑mortgage debt entirely and consider accelerated mortgage payments if your retirement savings trajectory is already on target. The key is matching liability duration with your career horizon; you don’t want a heavy debt load crossing into your late 60s. Also review big‑ticket lifestyle commitments—private schooling, luxury cars, second homes—through the lens of long‑term cash‑flow stress tests. Experts often model “what if” scenarios: job loss, health shock, market downturn. If your plan fails under these, your current lifestyle calibration is too aggressive and needs scaling back.

Health, Insurance and Human Capital Maintenance

Physically, this is when chronic conditions may start, so health‑related expenses trend upward. Upgrade your planning to include projected medical costs and potential long‑term care. Evaluate disability insurance adequacy because the probability of a partial work interruption rises in these decades. Also treat your skills as assets that can depreciate; allocate time and money to re‑skilling or up‑skilling so your employability remains strong into your 50s and beyond. Think of this as extending your earnings “runway,” which in turn gives you more flexibility in retirement timing and allows for higher resilience against portfolio volatility or temporary unemployment.

Your 50s: Transition From Accumulation to Decumulation Design

Pre-Retirement Stress Testing

In your 50s, the focus shifts from maximum growth to capital preservation and withdrawal strategy design. Perform detailed retirement simulations using multiple scenarios: early retirement, baseline retirement age and delayed retirement. This is the decade where retirement planning by age decade 20s 30s 40s 50s becomes highly specific to your portfolio size, pension rights and expected lifestyle. Experts recommend modeling sequence‑of‑returns risk—bad market years early in retirement—and adjusting asset allocation to cushion that risk. Consider partial annuitization or laddered bonds for predictable income, while keeping a growth component to hedge inflation over a potentially long retirement horizon.

- Define a clear retirement spending target with categories: essentials, wants, legacy.

- Plan debt‑free status by retirement date where possible.

- Align asset location (taxable vs tax‑advantaged) with withdrawal plans.

Fine-Tuning Investments and Withdrawal Logic

At this stage, the best investment strategies in your 20s 30s 40s and 50s converge on risk‑controlled diversification. Your equity weight may step down further, but not to zero—you still need growth to outpace inflation. Establish a structured withdrawal policy, such as a percentage‑based rule with guardrails that let you cut spending modestly after bad years. Coordinate this with Social Security or state pension timing, understanding the trade‑off between starting earlier at a lower benefit and delaying for a higher guaranteed payout. A specialized retirement planner can help you map tax‑efficient withdrawal sequences across account types and jurisdictions.

Legacy, Purpose and Safety Nets

Finally, zoom out from spreadsheets to purpose. Clarify what you want your money to do beyond funding daily living: support family, philanthropy, entrepreneurship or simply buying back your time. Update estate documents, beneficiary designations and healthcare proxies so they reflect current relationships and intentions. Evaluate whether long‑term care insurance, home modifications or geographic relocation could reduce late‑life risk and expenses. Periodically revisit your plan—markets, tax laws and your own priorities evolve. Understanding how to manage money at different ages 20s 30s 40s 50s isn’t a one‑time project but an ongoing iterative process tuned to each new phase of your life.