Most busy professionals don’t get into debt because they’re “bad with money”. It’s usually timing and complexity: variable bonuses, stock options, relocation costs, business travel on personal cards, kids, housing in expensive cities. You’re juggling calendars and KPIs, so debt becomes background noise until the interest pile is hard to ignore. The real challenge isn’t basic math; it’s building a system that fits a calendar full of calls, deadlines and unpredictability. Debt reduction strategies for busy professionals have to be low‑friction, automation‑friendly and tolerant of chaos, otherwise they die the same death as abandoned budgeting apps and unread bank emails.

Time-Poor, Debt-Rich: What Makes Busy Professionals Different

Your constraint is not income, it’s attention bandwidth. That changes the toolkit. Traditional advice says “track every expense”, but you’ll simply stop doing it mid‑quarter. Instead, think in terms of default settings: automatic overpayments scheduled for the day after payday, hard spending caps on cards, and pre‑decided rules that don’t require willpower every week. For some, debt consolidation services for professionals can simplify five or six credit lines into one predictable payment, even if the interest rate is only slightly better. The win is cognitive: fewer moving parts to forget. Any method you choose has to survive your worst weeks, not your most motivated weekends.

A practical test: if a method needs more than 10 minutes a week to maintain, assume you will abandon it and pick something simpler.

Classic Tactics: Snowball, Avalanche and Hybrid Approaches

Let’s compare the three main DIY strategies. The snowball method means you pay off the smallest balance first, regardless of interest rate, to get quick psychological wins. Avalanche targets the highest interest rate first, minimizing total interest paid. A hybrid approach blends both: you attack one or two small debts for quick momentum, then switch to the highest‑rate balances. For a senior consultant or manager with limited mental space, avalanche is usually more efficient but snowball is more emotionally sustainable. The question isn’t “which is theoretically best?” but “which will you actually maintain for 24 months without thinking about it daily?” Often the hybrid wins because it gives motivation early and efficiency later, matching how motivation tends to drop over time.

If you already have high income and stable employment, you can also combine these with targeted refinancing: use lower‑rate products to shrink interest, then apply avalanche or hybrid on the simplified structure.

Real Cases: How Professionals Actually Got Out of Debt

Case one: a 36‑year‑old software engineer with $48k in card and personal‑loan debt. She tried budgeting twice and quit both times. What worked was ruthless simplification. She rolled four high‑rate cards into a single personal loan, then used a hybrid strategy: first she crushed a small remaining store card for a quick win, then shifted to the new loan using automated biweekly overpayments set at 20% above the minimum. The technical detail that mattered: overpayments were tied to her base salary only, ignoring bonuses. Every bonus went 80% to principal, 20% to a “buffer fund” so new emergencies wouldn’t create debt again. It wasn’t heroic discipline; it was a rule that lived in the payroll system, not in her head.

Contrast that with a 42‑year‑old surgeon who refused consolidation because he valued flexibility. He kept separate cards for tax, travel and personal spending, but locked them behind hard limits and calendar reminders. Same goal, different constraints.

Non-Obvious and Alternative Methods

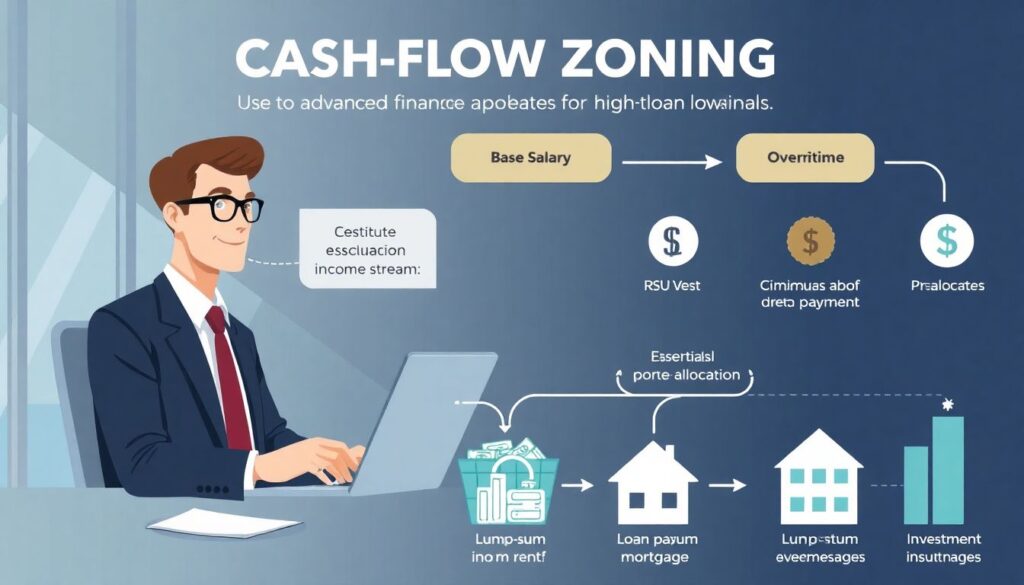

Beyond the classics, there are less obvious strategies that align with a demanding career. One is “cash‑flow zoning”: you treat each income stream differently. Base salary covers essentials and minimum payments, variable income (overtime, commission, RSU vests) is pre‑allocated to lump‑sum principal reductions. Another is behaviour‑based limits: instead of tracking coffee spend, you cap the number of active cards and recurring subscriptions. Some high earners get traction using the best debt relief programs for high income earners, which often bundle structured repayment, interest reductions and accountability check‑ins. These are not magic wands, but they create external pressure and a clear timeline. A more radical alternative is a short, aggressive cut in lifestyle for 6–12 months, treated as a “debt residency” period with a defined end date, rather than endless frugality.

If your stress is less about money and more about complexity, prioritize methods that reduce the number of decisions, even if they’re not mathematically perfect.

Pro-Level Hacks and When to Get Outside Help

Busy professionals underuse expert support. Think about credit counseling for busy professionals as a diagnostic, not a confession: a specialist can map all your liabilities, interest rates and contractual traps in one session and propose a sequence of moves you wouldn’t discover on your own. If your debt mix includes business obligations, tax arrears or old defaults, it may be rational to hire financial advisor for debt management who understands equity compensation, partnership distributions and corporate structures. For negotiations with banks or collectors, professional debt negotiation services can sometimes secure lower rates or settlements precisely because they speak the creditor’s language and know where the policy flexibility is. These options cost money, so compare their fees against the projected interest savings and time saved; for many high earners, the time factor alone justifies it.

On the lighter end, “hacks” look like calendarization and automation: set a 15‑minute monthly “money stand‑up” on your calendar, route all financial emails to a separate folder reviewed only then, and lock new debt behind friction, such as a 24‑hour wait before increasing any limit.

In the end, the “best” debt strategy is the one that matches your calendar, personality and risk profile. Choose a structure you can automate, add expert help where the stakes justify it, and treat debt reduction as a finite project with a clear end date, not a permanent identity.