Why Credit Cards Can Actually Make You Rich (If You Treat Them Like a Tool)

Most people see credit cards as traps.

Banks hope you’ll treat them like “free money” so you pay interest, late fees, and end up stuck.

You’re going to do the opposite: treat a credit card like a profitable tool, not a wallet extension.

This guide walks you through how to use credit cards responsibly to build wealth step by step, with real-world strategies, warnings, and a few non‑obvious tricks that most people never use.

—

Step 1. Reframe the Whole Game: You’re the Business, Not the Customer

When you use a card, the bank earns:

– fees from stores (interchange)

– interest from people who carry balances

– fees from people who pay late or mess up

Your goal is simple:

Use their system, collect rewards, build your credit score — and never pay them a cent in interest.

Think like a small business:

– Banks provide the infrastructure.

– You extract value (cashback, miles, protections, 0% promos).

– You track your “operations” like a spreadsheet, not like a shopping spree.

This mindset shift is the foundation of every strategy that follows.

—

Step 2. Pick the Right Card Setup Instead of “Whatever the Bank Offers”

Start Lean: One or Two Cards, Not a Pile

You don’t need 8 cards to win. For beginners, a simple setup is often the most powerful:

1. Primary daily card – for groceries, gas, subscriptions.

2. Backup card – in case the first gets blocked, plus different reward structure.

Later, you can layer in credit card strategies for maximizing rewards and travel points, but first you need control.

Choosing Cards with Strategy (Not by Shiny Ads)

Look for:

– No annual fee (at first).

– A simple cashback structure you’ll actually use.

– Decent customer service and app.

If you’re building or rebuilding credit, search for the best credit cards to build credit and earn rewards that don’t punish you with insane fees. As your score improves, you can upgrade, product change, or open better cards with higher limits and richer perks.

For long‑term planners who sometimes need to carry a balance (ideally rarely), consider the best low interest credit cards for long term financial planning, but treat them as emergency tools, not a standard habit.

—

Step 3. Create a “Card Usage System” Before You Swipe

Most people get in trouble not because they’re bad with money, but because they have no system.

Here’s a simple one.

1. Build an Automatic “Card Budget”

– Decide how much you can spend on your card per month without touching savings.

– Divide that by 4 to get a weekly cap.

– Every Sunday, check your card app. If you’re close to your weekly cap — you pause.

Short rule:

If you wouldn’t buy it with cash today, you don’t buy it with a card today.

2. Use a “Pre-Pay” Trick to Remove the Fear

Unusual but powerful move:

1. Before you start using a new card, send a small payment (e.g., $50–$100) even if the balance is zero.

2. Now any spending reduces that prepaid cushion first.

3. Mentally, you’re spending money you’ve *already* earmarked, not borrowing.

You can even link your card to a separate checking account used only for card payments and fund it weekly. That keeps your main savings insulated.

3. Turn “Paying the Card” into a Weekly Ritual

Instead of waiting for the statement date, do this:

– Once a week, log in and pay off everything you spent last week.

– Treat it like rent — non‑negotiable.

Paying frequently has perks:

– Keeps your balance low (good for your score).

– Stops “surprise” big bills.

– Trains your brain that the card is just a faster way to move your money, not extra money.

—

Step 4. Understand How Your Credit Score Really Moves

If you’re wondering how to use credit cards responsibly to improve credit score, it comes down to a few main levers — and most of them are in your hands.

Key Factors You Control

1. On‑time payments

Even one 30‑day late mark can haunt you for years. Autopay at least the minimum on every card, always.

2. Utilization (how much of your limit you use)

– Aim to report under 30% of your total available limit.

– Under 10% gives you even better results.

– Example: You have a $1,000 limit. Try to keep your reported balance under $100–$300.

3. Age of credit

The longer your accounts stay open (in good standing), the better. Avoid closing your oldest no‑fee card.

4. New inquiries

Each new card application adds a hard inquiry. Space them out; no need to rush.

When you combine low utilization, on‑time payments, and patience, your score tends to rise steadily and quietly in the background.

—

Step 5. Turn Everyday Spending into Profit

Use Rewards as a Rebate, Not a Coupon to Spend More

Think of rewards like a rebate — you’d have spent that money anyway.

If you pick high cash back credit cards for everyday spending, you can effectively get a small percentage discount on your life:

– Groceries

– Gas and transit

– Phone/internet bills

– Streaming services

Key rule:

No “I’ll buy it because I get points.” Points are not a discount if you purchase something you didn’t need.

Build a Simple “Rewards Stack”

Once you’re comfortable, you can get clever:

1. Use a card that gives bonus points on groceries for your supermarket runs.

2. Use another that gives extra points on travel for flights and hotels.

3. Use a flat‑rate cashback card for everything else.

Over time, this becomes your personal set of credit card strategies for maximizing rewards and travel points — without spreadsheets or stress.

—

Step 6. Non‑Standard Tricks to Quietly Grow Wealth

Now for some less common, but still responsible, strategies.

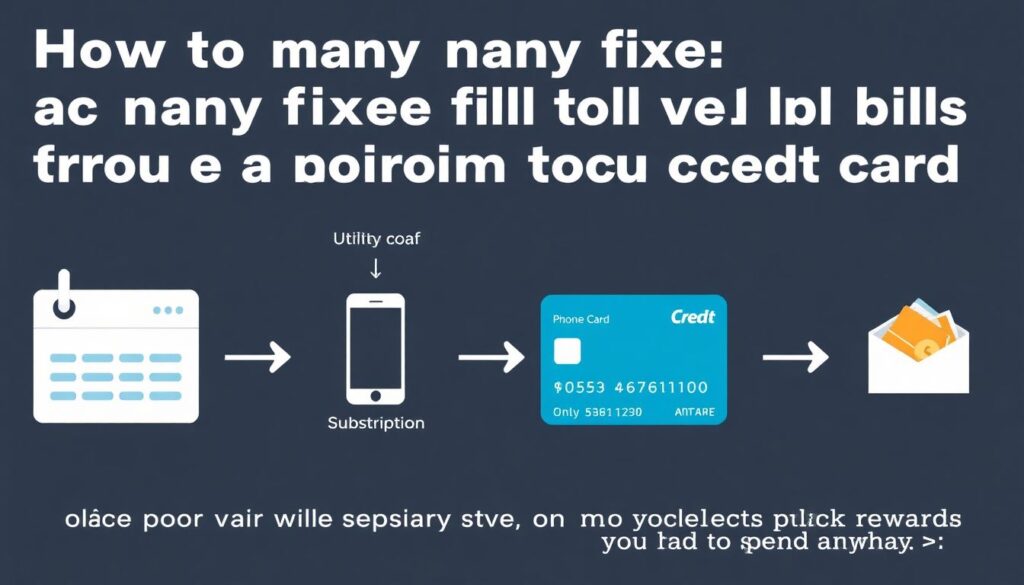

1. The “Bill Funnel” Strategy

Route as many fixed bills as possible through your card:

– Utilities

– Phone plan

– Subscriptions

– Insurance premiums (if there’s no extra fee)

Then:

– Autopay those same bills from your checking account to the card every month.

– You collect rewards on money you had to spend anyway.

– Your payment history becomes rock solid and predictable.

Result:

You’re building credit and earning rewards on autopilot.

2. The “Savings Match” Move

Every time you earn cashback:

1. Check how much you’ve earned this month (say $25).

2. Transfer the same amount from checking into savings or investments.

3. Redeem the $25 cashback as normal.

Effect:

You’ve turned $25 in rewards into $50 in real wealth growth — part from the bank, part from your commitment.

Over a year, that habit can quietly move hundreds of dollars into savings or an investment account.

3. “Future You” Emergency Buffer

Use a credit card as an emergency‑only backup, not as your first line of defense:

– Keep a real cash emergency fund (even if small).

– Reserve part of your card limit as a last resort, not as spending money.

If you ever have to use it for a real emergency:

– Immediately build a repayment plan.

– Temporarily stop non‑essential card spending until it’s paid off.

You’ve turned the card into a safety net, not a lifestyle booster.

4. Strategic 0% APR — With an Exit Plan

Some of the best low interest credit cards for long term financial planning come with 0% APR promos on purchases or balance transfers.

Used carefully, they can help:

– consolidate higher‑interest debt

– spread out a planned, necessary expense (like a move or car repair)

But you must:

– divide the total by the number of promo months

– set auto‑payments to clear it before the promo ends

No plan, no promo. That’s the rule.

—

Step 7. Travel and Big Purchases Without Getting Burned

Using Cards for Travel the Smart Way

Cards can give you:

– trip protections

– no foreign transaction fees

– better exchange rates

– travel insurance (on some cards)

If you’re chasing flights and hotels, focus your credit card strategies for maximizing rewards and travel points on:

– cards that earn points on travel and dining

– flexible points you can move to airlines or hotels

– using points for *high‑value* redemptions (like long‑haul flights)

But always ask:

> If I had to pay this in full today in cash, would I still book this trip?

If the answer is no — the trip is too expensive for you right now.

Big Purchases: When a Card Helps, When It Hurts

A big purchase on a card makes sense when:

– You already have the cash saved, and

– The card gives extended warranty or purchase protection, and

– You’re earning meaningful rewards on it.

It doesn’t make sense when:

– You’re hoping “future you” will figure it out later.

– You’re already carrying a balance.

If it takes more than 3–6 months to repay without stress, rethink the purchase.

—

Step 8. Common Traps to Avoid (So You Don’t Undo Your Progress)

1. Chasing Every Signup Bonus

Yes, some of the best credit cards to build credit and earn rewards come with tempting welcome offers.

But if you:

– open too many cards too fast

– lose track of due dates

– overspend just to hit “spend $3,000 in 3 months”

…you’ll wipe out any gains with debt and fees.

Stick to a limit:

No more than 1–2 new cards a year, and only if they fit a clear purpose.

2. Ignoring the Fine Print

Always know:

– Annual fee (and when it posts)

– Regular APR after promos

– Foreign transaction fees

– Penalty APR if you pay late

You don’t need to memorize the whole agreement — just understand the parts that cost you money.

3. Treating “Available Credit” as “Available to Spend”

If your card limit jumps from $1,000 to $5,000, nothing in your life actually changed.

– Your budget did not grow.

– Your income did not increase.

Higher limits are mainly for:

– lowering utilization (good for credit score)

– handling genuine emergencies

– smoothing large planned purchases that you can repay quickly

—

Step 9. A Simple 9‑Point Checklist for Responsible Credit Card Use

Use this as a quick mental model:

1. Always pay on time. Put autopay on at least the minimum; aim to pay in full.

2. Keep utilization low. Try to stay under 30% of your limit; under 10% is even better.

3. Budget first, swipe second. If it’s not in your monthly plan, it’s a maybe — not a yes.

4. Check your account weekly. Look for weird charges and track spending.

5. Use rewards on needs, not random splurges. Or pair them with the “savings match” move.

6. Avoid carrying balances. If you’re consistently not paying in full, slow down spending.

7. Add cards slowly. Each new card should have a solid reason to exist.

8. Never spend “for the points.” Rewards are a bonus, not a justification.

9. Treat your card like a debit with benefits. You only use money you already have.

—

Step 10. Connect Credit Cards to Your Bigger Wealth Plan

Using cards well doesn’t make you rich alone. It does something more important:

– Lowers your borrowing costs (via a better score).

– Protects you from random financial hits (with card protections).

– Applies a small “discount” across most of your regular spending (via rewards).

– Helps you practice discipline, budgeting, and delayed gratification.

The real wealth comes from what you do with the freed‑up cash:

– Paying down high‑interest debt faster.

– Boosting your emergency fund.

– Investing regularly in index funds, retirement accounts, or your business.

– Avoiding expensive personal loans because your credit score is strong.

Use credit cards as leverage for your existing goals, not as the goal itself.

—

Final Thought

If you:

– pay in full

– stay organized

– treat every swipe as spending your own money

…credit cards become a quiet engine in your financial life — improving your credit score, padding your savings, and shaving costs off things you’d buy anyway.

That’s how to use credit cards responsibly to build wealth: not by playing a flashy game, but by running a calm, controlled system where you call the shots and the bank’s tools work for you.