Why Health Insurance Feels So Complicated (And Why You Can Handle It)

Understanding your health insurance is basically learning a new mini-language: premiums, deductibles, copays, coinsurance, out‑of‑pocket maximums, networks. It sounds dense, but once you map the terms to real money and real situations, it becomes much more predictable.

Think of your policy as a rulebook about who pays what, when, and under which conditions. This guide walks you through that rulebook step by step, in plain language, with real cases and a few technical terms you actually want to know.

—

H2: Core Concepts You Need Before Anything Else

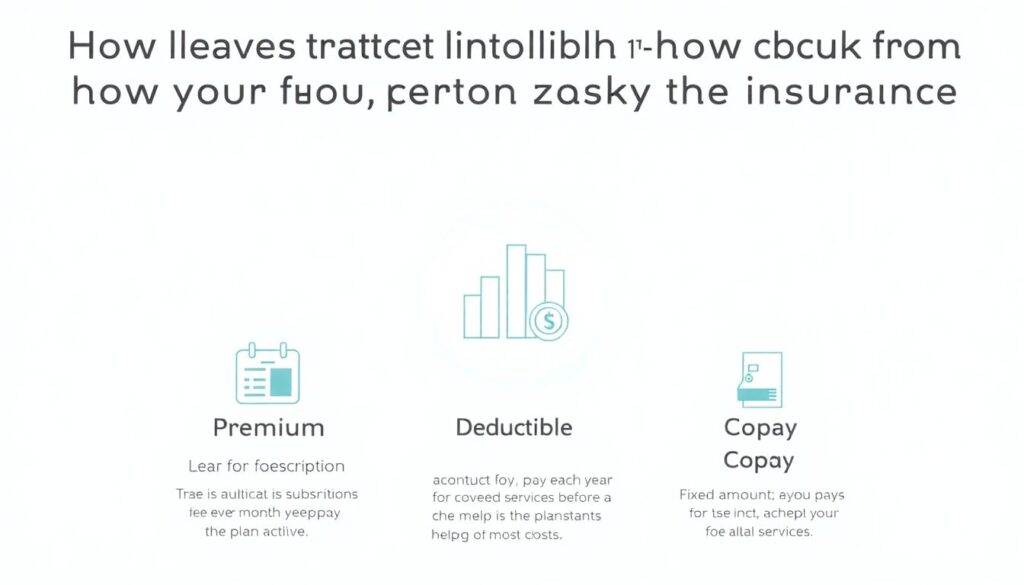

H3: The Four Money Streams in Your Policy

Let’s start with the four main levers that control how much you actually pay:

– Premium – The subscription fee you pay every month to keep the plan active.

– Deductible – The amount you pay each year for covered services before the plan really starts helping with most costs.

– Copay – A fixed amount you pay for a service (e.g., $30 per doctor visit).

– Coinsurance – A percentage of the cost (e.g., the plan pays 80%, you pay 20%).

Here’s health insurance deductible vs copay explained in one sentence:

Your deductible is a yearly threshold; your copay is a per‑visit or per‑service ticket price. They can exist together: you may pay full price toward your deductible first, and *then* switch to predictable copays once you’ve met it.

H3: Network, Formulary, and Prior Authorization

Short version: the plan rewards you for staying inside its system.

– Network – The doctors and hospitals that have pre‑negotiated rates with your insurer.

– Formulary – The official list of medications your plan covers and how it covers them.

– Prior authorization – Advance approval your doctor must get from the insurer for certain tests, drugs, or surgeries.

If you see an out‑of‑network specialist, the math can change drastically: a $200 in‑network visit could easily become an $800 out‑of‑network bill, with a different deductible and higher coinsurance, or no coverage at all.

—

H2: Necessary Tools and Documents

H3: Paper and Digital Tools You Actually Need

To work with your insurance like a pro, gather these items first. It’s your “control panel”:

– Full policy document (Certificate of Coverage / Evidence of Coverage) – The long PDF with all the rules, not just the one‑page summary.

– Summary of Benefits and Coverage (SBC) – The 2–4 page snapshot: premiums, deductibles, copays, coinsurance, and out‑of‑pocket maximum.

– Provider directory – Searchable list of in‑network doctors, labs, and hospitals.

– Drug formulary – Shows which tier your medications fall into and what you’ll pay.

Keep these in a cloud folder or email search label. You’ll reference them more than you think—especially when a bill doesn’t look right.

H3: Helpful Apps and Online Accounts

Don’t skip the tech tools; they save time and prevent errors:

– Insurer’s online portal or app – Check claims, track what you’ve paid toward your deductible, download letters, and find in‑network providers.

– Telehealth app – Often cheaper and faster for common issues (rashes, UTIs, mild infections).

– Personal notes app or spreadsheet – Log every call: date, time, person’s name, and what they promised.

If you’re hunting for affordable health insurance plans for individuals, many marketplaces (government and private) have calculators and “side‑by‑side” views. Use them like you would a flight comparison site—same idea, just more jargon.

—

H2: Step‑by‑Step: From Choosing a Plan to Using It

H3: Step 1 – Decide What You Actually Need

Before doing a health insurance plans comparison, do a quick self‑assessment. Over a typical year:

– How many doctor visits do you usually have?

– Any planned surgeries, pregnancy, or ongoing physical therapy?

– Do you take regular brand‑name medications?

– Are your favorite doctors or clinics must‑keep?

Now map yourself roughly into one of these usage patterns:

Low use, moderate use, or high / complex use. This matters more than people realize.

H3: Step 2 – Compare Plans the Right Way

When you look at options, don’t just ask “What’s the cheapest premium?” Ask, “What’s my likely total yearly cost?”

For each plan, estimate:

1. Total annual premiums – Monthly premium × 12.

2. Expected care costs – Rough value of your visits, drugs, and tests.

3. How those costs hit your deductible and copays – Does the plan cover some visits before the deductible? Are generics cheap?

In other words, how to choose health insurance plan is really:

Minimize your total (premiums + out‑of‑pocket) for *your* pattern of care, not some imaginary normal person.

If you have frequent appointments or expensive drugs, a higher premium with a lower deductible and better coinsurance can be one of the best health insurance coverage options even though it “looks” more expensive per month.

H3: Case: Two Similar‑Paying Jobs, Two Very Different Plans

– Lena chooses a low‑premium, high‑deductible plan because she’s healthy and only does annual checkups. She ends the year having paid premiums plus about $150 in occasional visits—her strategy works.

– Tom, same company, same salary, chooses the same plan but has a surprise knee surgery. He hits a $6,000 deductible and 20% coinsurance on top. For him, a mid‑tier plan with higher premiums but a $1,500 deductible would have been cheaper overall.

The lesson: a health insurance plans comparison that only looks at monthly price is incomplete. You’re buying a risk‑management tool, not a subscription box.

H3: Step 3 – Enrollment and Verification

Once you pick a plan:

– Complete the enrollment on your employer’s portal or the public marketplace.

– Confirm:

– Your effective date (when coverage starts).

– That your primary doctor and key specialists show as in‑network *for that specific plan*.

– That your major medications appear on the formulary at acceptable tiers.

Save the confirmation screens and any reference numbers. Take screenshots. If something goes wrong later, this is your proof.

H3: Step 4 – Using the Plan Day‑to‑Day

When you actually seek care:

1. Verify network status

Call the clinic or check the insurer’s site:

“Can you confirm you’re in‑network for [Insurer] [Plan Name] for 2025?”

2. Ask about cost before the visit when possible

Use phrases like:

– “Is this coded as preventive care?”

– “Roughly what does this cost self‑pay vs through insurance?”

3. At the pharmacy

Check if there’s a cheaper generic. Ask if using a discount card (without insurance) is cheaper than your copay. Surprisingly often, it is.

4. After the visit

You’ll first get an Explanation of Benefits (EOB) from your insurer, *not* a bill. That document shows:

– What the provider charged.

– What the insurer allowed.

– What the insurer paid.

– What you owe.

Only pay *after* the provider’s bill matches the EOB. If they don’t match, pause and investigate.

—

H2: Troubleshooting Common Problems

H3: Problem 1 – Surprise High Bills

Case: David’s “free” colonoscopy

David scheduled a routine screening colonoscopy. Preventive screenings are typically paid at 100% with no deductible. After the procedure, a small polyp was removed and sent to pathology.

Weeks later, David receives a $1,200 bill because the visit was coded as “diagnostic” rather than “preventive.”

How he fixed it:

1. David pulled his Summary of Benefits and confirmed colon cancer *screening* is preventive, fully covered.

2. He called the gastroenterologist’s billing office and asked for:

– The procedure codes (CPT/HCPCS) and diagnosis codes (ICD‑10).

– Confirmation of how they coded preventive vs diagnostic.

3. Armed with codes and policy language, he called his insurer and requested a review, pointing out that a polyp found during a screening shouldn’t automatically convert everything to diagnostic.

After a re‑review, the claim was partially recoded as preventive, reducing the bill sharply.

Your checklist when this happens:

– Compare the provider’s bill with the EOB.

– Confirm whether the service should be preventive per your policy.

– Ask the provider to review and, if warranted, recode the claim.

– Then ask the insurer to reprocess it.

H3: Problem 2 – Denied Claims

Case: Maya’s denied MRI

Maya’s doctor ordered an MRI for persistent back pain. The claim was denied as “no prior authorization.”

What she did:

– Called the doctor’s office to confirm whether they’d requested prior authorization. They hadn’t—they assumed it wasn’t needed.

– Asked the office to submit a retroactive authorization request, including clinical notes.

– Called the insurer to note on the file that her doctor was submitting documentation.

Result: the insurer approved the MRI retroactively. Maya still paid her share under the plan rules, but not the full cash price.

If your claim is denied:

– Ask for the reason code and the specific rule used (e.g., “no prior auth,” “out of network,” “not medically necessary”).

– Get copies of all related clinical notes from your doctor.

– Ask the doctor to support a medical necessity appeal, if appropriate.

– File an appeal within the deadline; note dates and names of everyone you speak with.

H3: Problem 3 – “I Thought This Doctor Was In‑Network”

Case: Sam’s emergency room bill

Sam went to an in‑network hospital ER. The hospital itself was in‑network, but the ER doctor group was out‑of‑network, and the radiologist reading his scan was also out‑of‑network. He got multiple surprise bills.

How he pushed back:

– He checked his state’s surprise billing / balance billing protections and found that emergency services at in‑network facilities can’t bill him above in‑network rates.

– He called the insurer, cited the law, and asked them to reprocess the claim as in‑network under surprise billing rules.

– He called the ER physician billing office, gave them the insurer’s updated processing details, and refused to pay more than the in‑network cost‑share.

Eventually, the extra charges were written down to in‑network levels.

—

H2: Real‑World Case Studies: Matching Plans to Real Lives

H3: Case 1 – The Freelancer Hunting for Affordable Coverage

Profile:

Alice, 34, freelance designer, no major health issues, a few urgent care visits over the last five years, takes one generic medication.

She’s searching marketplaces for affordable health insurance plans for individuals. At first, she’s drawn to the lowest premium possible. But after she runs the numbers:

– Plan A: Very low premium, $8,000 deductible, no copays until deductible.

– Plan B: Moderate premium, $2,500 deductible, $25 primary‑care copay, $10 generic drugs from day one.

Alice estimates:

– 2 primary‑care visits

– 1–2 urgent care visits

– Yearly prescriptions

– Maybe one surprise issue

She calculates that, even in a “medium‑bad” year, Plan B’s higher premium plus lower visit costs is only slightly more expensive—but gives her better protection if something big happens.

Given her risk tolerance, she picks Plan A *only if* she commits to saving in a health savings account (HSA). Otherwise, Plan B is safer.

H3: Case 2 – The Family with Predictable but Frequent Use

Profile:

Mark, 42, spouse, two kids. One child has asthma; his spouse has regular physical therapy.

They’re comparing options through Mark’s employer, trying to find the best health insurance coverage options for routine, frequent care.

They list expected annual services:

– ~8–10 pediatric visits (colds, infections, follow‑ups).

– Monthly asthma inhalers and occasional ER visits.

– Weekly PT for 3 months.

They focus on:

– Pediatric and specialist copays.

– Asthma medication tiers in the formulary.

– Physical therapy visit limits and copays.

Their how to choose health insurance plan process is deliberate: they estimate a bad‑case year under each plan. The plan with slightly higher premiums but lower pediatric and PT copays saves them hundreds overall and smooths out cash flow, so they choose that one.

H3: Case 3 – The Chronic‑Condition Professional

Profile:

Sara, 50, has rheumatoid arthritis, sees a specialist every few months, and takes a biologic medication that’s extremely expensive without insurance.

Her priorities:

– Low specialty‑drug copays or coinsurance.

– Strong specialist network.

– Lower out‑of‑pocket maximum, even if premiums are higher.

During her health insurance plans comparison, she finds:

– One plan with low premiums but 40% coinsurance on specialty drugs.

– Another with higher premiums, fixed copays for specialty drugs after a reasonable deductible, and a lower annual out‑of‑pocket maximum.

Given her high predictable costs, she optimizes for maximum protection rather than minimum premium. Over the year, the higher‑premium plan actually saves her thousands.

—

H2: Final Checks Before You Commit (And Every Time You Use Care)

H3: A Simple Pre‑Visit Checklist

Use this quick list every time you schedule care:

– “Are you in‑network for my exact plan name?”

– “Does this service usually require prior authorization?”

– “Is this preventive, or will it apply to my deductible?”

– “What will you bill as the procedure code if you know it?”

And after:

– Match every bill to your EOB before paying.

– If something looks off, call *politely but firmly* and ask:

– “Can you walk me through how this was coded?”

– “Can you explain how my benefits were applied?”

—

Understanding your health insurance is less about memorizing jargon and more about knowing which levers to pull and which questions to ask. With the right documents, a bit of structured health insurance plans comparison, and the troubleshooting steps above, you can turn a confusing system into something you actively manage—rather than something that just happens to you.