Most people don’t avoid money planning because they’re lazy; they avoid it because it feels complex, abstract and a bit scary. A simple 5‑year financial plan turns that vague anxiety into a concrete roadmap — numbers, dates, and clear next steps. Let’s walk through how to do that in plain language, compare different approaches, and see how real people use this to move from “I have no idea what I’m doing” to “I know exactly what happens with my money next month and next year.”

—

Step 1: Translate “I want to be better with money” into specific 5‑year targets

The first switch from overwhelmed to organized is moving from fuzzy wishes to measurable objectives. In financial planning terms, you’re defining your *strategic goals* and *time horizon*.

Instead of “I want to save more,” define numbers and dates:

– Build a 6‑month emergency fund by December 2027

– Pay off all credit cards within 24 months

– Save $40,000 for a home down payment in 5 years

– Invest $300/month for long‑term wealth accumulation

At this stage, don’t worry about *how*. Your task is to decide *what* matters in the next five years so your 5‑year financial plan isn’t just a spreadsheet; it’s a translation of your real life into cash flows and milestones.

—

Step 2: Three main approaches — DIY, guided templates, and working with a pro

There isn’t one “correct” way to build a plan. People usually fall into one of three camps:

– Pure DIY (spreadsheet and willpower)

– Using a 5 year financial plan template or planning app

– Collaborating with a professional financial planner

Each approach has strengths and trade‑offs in terms of control, cost, and depth of analysis.

—

DIY planning: maximum control, minimum structure

The DIY route is simple: open a blank sheet, list income, expenses, debts, and goals, and try to map everything for 60 months.

This approach suits people who:

– Enjoy working with numbers

– Are comfortable researching terms like “compound annual growth rate” or “debt snowball”

– Have relatively straightforward finances (1–2 income sources, a few accounts, limited debt)

The main risk of pure DIY is hidden blind spots. It’s easy to skip tax implications, underestimate irregular expenses, or forget about inflation and interest rate changes. The result often looks organized but fails under real‑world stress.

—

Using a 5 year financial plan template: structure without a steep learning curve

A balanced middle ground is to start with a structured 5 year financial plan template. This might be a downloadable spreadsheet, a Notion page, or an in‑app template. Instead of staring at a blank screen, you get ready‑made sections for:

– Net worth snapshot (assets vs. liabilities)

– Income and expense categorization

– Debt payoff timelines

– Savings and investment goals

– Scenario analysis (“what if I increase investing by $100/month?”)

For many people, this instantly reduces overwhelm. The template acts like a checklist: if there’s a field for it, you’re reminded to think about it. You still own the numbers and decisions, but you’re not reinventing the wheel every time you adjust your plan.

—

Software‑driven approach: automation and “what‑if” tools

If you want more analytics, the next step up is using the best financial planning software for individuals you can reasonably learn. Modern tools can:

– Sync transactions automatically from bank and investment accounts

– Categorize expenses with machine learning

– Run projections showing how your net worth might evolve over five years

– Model different contribution rates, rate‑of‑return assumptions, and inflation scenarios

Compared to a static template, software fits people who like dashboards and simulations. The drawback: a learning curve and sometimes subscription costs. If you’re not willing to invest a few hours understanding the interface and assumptions, the tool will feel overwhelming rather than liberating.

—

Working with a planner: outsourcing complexity, keeping ownership

When your situation includes business income, stock compensation, several loans, or upcoming life changes (kids, relocation, immigration issues), it can be rational to hire financial planner for long term goals and use their expertise as a decision‑support system.

This doesn’t mean giving up control of your money. A good planner:

– Builds a structured, customized 5‑year roadmap

– Integrates taxes, risk management, and investment strategy

– Reviews your plan annually and after big life events

Many people search for “personal financial planning services near me” expecting a sales pitch, but the better firms operate more like consultants: they charge for advice, not just for selling you products. The trade‑off is cost, but done right, a planner saves you from expensive mistakes that exceed their fee.

—

How to create a 5 year financial plan: a simple, repeatable workflow

Regardless of whether you go DIY, template‑based, software‑driven, or with a planner, the core workflow is the same. Think of it as a loop, not a one‑time task:

1. Diagnose your starting point

– List all accounts, balances, debts, interest rates, and recurring obligations.

– Capture your true monthly average spending, not your “ideal” spending.

2. Define and rank goals

– Short‑term (0–2 years): emergency fund, debt stabilization.

– Medium‑term (3–5 years): home down payment, career re‑training, starting a business.

3. Design your cash‑flow engine

– Decide how much goes to fixed costs, flexible costs, debt, and investments.

– Embed “pay yourself first” as an automatic monthly transfer.

4. Run 5‑year projections

– For each year, estimate: debt balances, savings balances, and net worth.

– Stress test: what if income drops by 20% for six months?

5. Automate and monitor

– Set automatic transfers and debt payments.

– Add a recurring calendar event: “Monthly 30‑minute money review.”

This loop is the backbone. The tools and helpers you choose just change *how* you execute it.

—

Inspiring examples: from vague anxiety to concrete progress

Consider three short, realistic case sketches that highlight different approaches.

Case 1: The spreadsheet minimalist

Anna, 27, had two credit cards, a small student loan, and no savings. She used a simple spreadsheet (DIY plus a basic online template) to:

– List debts by interest rate

– Assign every dollar of her paycheck a “job” (fixed costs, debt, future self)

– Apply the *avalanche* method, paying extra on her highest‑interest card

In five years, she:

– Cleared all consumer debt

– Built a four‑month emergency fund

– Started contributing 15% of income to retirement

Her approach was low‑tech, but her discipline and monthly reviews made it effective.

—

Case 2: The software‑driven optimizer

Marcus, 35, worked in tech, received stock compensation, and wanted to plan for buying a home and maybe starting a company. DIY felt too risky. He chose one of the best financial planning software for individuals he could find and upgraded to a paid tier. The software helped him:

– Model three scenarios: stay employed, join a startup, or freelance

– Estimate tax impact of exercising stock options

– Set target savings milestones for each path

Over five years, he didn’t just buy a home; he timed his stock sales and tax payments strategically, avoiding a cash‑flow crunch. The software didn’t decide for him; it made the trade‑offs visible.

—

Case 3: Combining planner expertise with personal ownership

Leah and David, a couple in their early 40s with two kids, had multiple income streams, a mortgage, and aging parents. They tried a template and got stuck on questions about insurance coverage and college funding. They decided to work with a planner instead of continuing to guess.

Their planner:

– Consolidated fragmented accounts into a coherent net‑worth picture

– Built a 5‑year and 15‑year dual‑horizon plan (kids’ education and their retirement)

– Recommended a priority order: stabilize emergency fund → optimize insurance → accelerate mortgage payments → invest for college

Five years later, they didn’t “get rich quick,” but they:

– Eliminated high‑rate debt

– Fully funded a 6‑month emergency reserve

– Opened education accounts with automated contributions

The planner was the architect; they were the builders executing the plan.

—

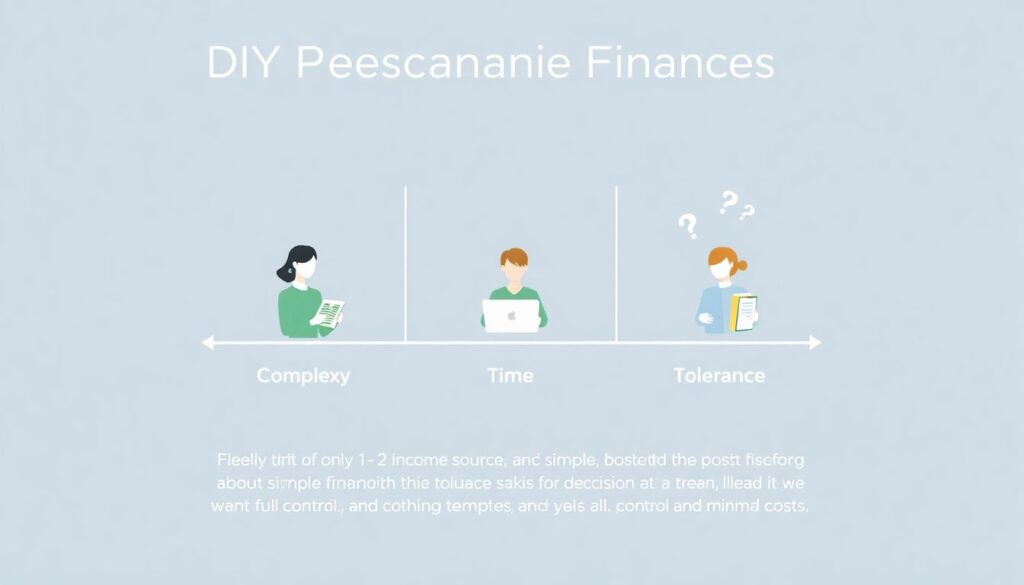

How to choose your planning approach: a quick comparison

Think in terms of three variables: *complexity*, *time*, and *tolerance for uncertainty*.

DIY might be enough if:

– You have 1–2 income sources and straightforward goals

– You’re willing to spend time learning basic financial concepts

– You prefer full control and minimal costs

Templates or apps are better if:

– You want structure but don’t need deep tax/legal advice

– You like visual dashboards and guided forms

– You want to reduce manual data entry and errors

Professional guidance makes sense if:

– You juggle business income, equity, cross‑border issues, or large upcoming decisions

– The cost of a bad decision (tax penalties, missed benefits, poor investment structure) is high

– You want an accountability partner as well as technical advice

You can also mix approaches: start with a template, layer in software, then schedule a targeted session with a planner for complex questions.

—

Recommendations for personal development through money planning

Building a 5‑year financial plan is also a way to upgrade your skills and mindset. Treat it as developing *financial literacy* and *decision‑making competence*, not just moving numbers around.

Focus on these development areas:

– Numeracy and data habits: learn to read basic financial statements, understand interest, and track trends instead of isolated numbers.

– Behavioral awareness: notice which spending triggers sabotage your plan; design friction (e.g., 24‑hour delay before large purchases).

– Strategic thinking: practice asking, “What does this decision do to my 5‑year picture?” before saying yes.

Each monthly review is a micro‑training session. Over time, your identity shifts from “I’m bad with money” to “I manage a personal financial system.”

—

Resources and learning paths to support your 5‑year plan

You don’t need a finance degree, but you do need a learning strategy. Combine three types of resources:

– Foundational knowledge

– Short online courses on budgeting, investing basics, and debt management

– Well‑reviewed, evidence‑based personal finance books (avoid “get rich quick”)

– Tools and templates

– A starter 5 year financial plan template from a reputable source (non‑promotional, transparent assumptions)

– Budgeting and tracking apps that integrate with your bank

– Specialist input

– Fee‑only advisors or planners for one‑time plan reviews

– Niche communities (forums or groups) aligned with your situation: freelancers, immigrants, young families, late‑career switchers

If you’re unsure whether to look online or locally, you can search personal financial planning services near me and then cross‑check credentials, fee structure, and conflict‑of‑interest policies.

—

From chaotic to clear: what “organized” actually looks like in five years

Being “organized” with money doesn’t mean perfection. It means:

– You know your exact monthly obligations and savings rate.

– You can open a document or app and see where you stand against your 5‑year targets.

– When something unexpected happens, you have a protocol: check emergency fund → adjust contributions → re‑run your 5‑year projection.

The fear doesn’t entirely disappear, but it’s no longer running the show. You have a structure, a method, and a realistic sense that if you stick to the process — whichever approach you choose — five years from now you’ll be looking back at today as the moment you stopped guessing and started planning.