Why a Busy Mom Needs Her Own Money Playbook

Being a busy mom means your time, energy, and money are all under pressure. A personal finance plan is basically a written playbook that tells your money what to do before chaos hits. Instead of reacting to surprise bills, school fees, or car repairs, you create a simple system that runs in the background. Think of it as a personal finance planner for moms that fits between daycare drop‑off, work, and bedtime stories, not a complicated spreadsheet that eats your weekends.

Necessary Tools and Setup

Start with just a few core instruments: one place to see all accounts, one method to track spending, and one calendar for due dates. Many women overcomplicate the stack: five apps, multiple notebooks, random screenshots. Pick one “source of truth” and build around it. For example, you can use a paper notebook plus the best budgeting app for busy moms that syncs bank data and sends alerts when you’re close to your limit in groceries, kids’ activities, or household supplies.

Use tools that cut manual work:

– Banking app with instant balance and push notifications

– Budgeting or cash‑flow app with automatic categorization

– Shared calendar for bill dates, renewals, and savings transfers

If you’re not comfortable with numbers, an online personal finance course for moms can help you understand terms like “cash flow”, “sinking fund”, and “debt‑to‑income ratio” without boring lectures. Keep a simple folder (digital or physical) for salary slips, insurance policies, loan contracts, and major receipts. This reduces stress when you review your plan or speak with a professional, and it helps you see patterns instead of isolated payments.

Step‑by‑Step Planning Process

Step one: map your current cash flow. Pull the last two or three months of statements and group expenses into 6–8 big buckets: housing, food, transport, kids, debt, health, and “everything else”. Don’t chase perfect categorization. You just need a clear view of where money leaks out. This is your starting data, not a verdict on your character. You’ll probably notice 2–3 categories that look inflated; that’s where your first optimizations will come from.

Step two: define non‑negotiables and goals. Non‑negotiables include rent or mortgage, basic food, childcare, minimum debt payments, and key insurance. Then set three explicit goals: one short‑term (e.g., build a $500 emergency buffer), one mid‑term (pay off a credit card), and one long‑term (college fund or house down payment). Writing them down gives your budget a direction, so you’re not just “trying to spend less” but reallocating cash toward something that matters to your family.

Step three: build a practical spending plan. Use a simple framework: income minus essentials, then automate goals, then allow flexible spending. For instance, set automatic transfers the day after payday to savings and debt; whatever remains is your flexible pool. Many moms benefit from digital “envelopes”: separate sub‑accounts for groceries, kids, and fun. If you feel stuck, you can hire financial advisor for family budget planning just for a one‑time session to sanity‑check your numbers and make sure insurance and retirement are not ignored.

Consider this action checklist:

– Automate bill payments and savings transfers right after payday

– Create 2–3 “goal” sub‑accounts (emergency, debt, kids’ costs)

– Cap variable categories (e.g., restaurants) with app‑based limits

If you’re parenting solo, investigate financial planning services for single moms through local nonprofits, credit unions, or community centers. They often provide low‑cost or free sessions, help restructure debt, and explain benefits you may be missing. Having a professional map out child support, government programs, and tax credits can significantly improve your monthly cash flow without adding more working hours.

Real‑Life Cases from Practice

Case 1: Emma, a nurse with two kids, was constantly overdrafting even though her income looked solid on paper. Her turning point came when she realized that school‑related expenses—sports, field trips, clothing—spiked irregularly and destroyed her monthly budget. We created a “kids sinking fund”: she set aside a fixed $120 every month into a separate sub‑account. Within three months, overdraft fees disappeared because the money for those “surprise” school costs was already parked and labeled.

Case 2: Laura, a married software engineer, felt guilty for ordering takeout several times a week. Instead of banning takeout, we quantified it. Her household decided on a fixed “convenience budget” of $200 a month for anything that saves time: meal kits, ride‑shares, house cleaning. They tracked it inside a budgeting app and treated it like a tool, not a shameful secret. Stress dropped, arguments about money decreased, and they still increased retirement contributions by redirecting just part of their previous random spending.

Case 3: Nina, a single mom in grad school, juggled part‑time work and childcare. She assumed she could not save at all. Together we reviewed her transactions and identified unused subscriptions, overpriced phone plans, and duplicated streaming services shared with relatives. We freed about $90 per month and split it between a starter emergency fund and an annual train pass that lowered commuting costs. After six months, she had a small but real buffer that kept a broken laptop from turning into new credit‑card debt.

Troubleshooting and Staying on Track

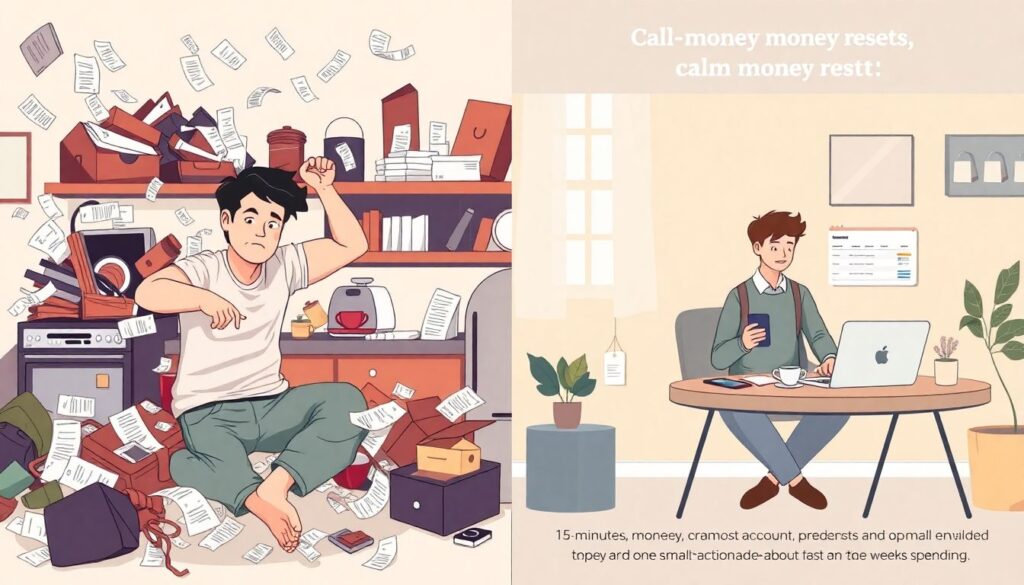

The most common failure point is “all‑or‑nothing” thinking. A chaotic week hits—sick child, overtime, no energy to cook—and the budget gets ignored. Instead of restarting from zero, use a weekly 15‑minute “money reset”: check balances, move small amounts back into place, and decide one micro‑adjustment for next week. Even a $10 transfer to savings keeps the habit alive. Your plan should survive real life, not rely on perfect discipline or unlimited willpower.

When your situation changes—new baby, job loss, divorce—treat it as a version update, not a collapse. Temporarily switch to “stability mode”: focus on paying essentials, protecting your credit score, and keeping a tiny emergency reserve intact. Pause extra debt payments if needed and communicate with lenders early. Many busy women worry that asking for help is a weakness, but using community aid, employer benefits, or a short consultation with a planner is simply rational resource management, not a personal failure.