Historical Background

Investment statements, as we know them today, are a relatively modern phenomenon. In the early 20th century, investors relied heavily on brokers for verbal or handwritten updates. The lack of transparency often led to confusion, overcharges, or fraud. With the rise of regulatory bodies like the U.S. Securities and Exchange Commission (SEC) in the 1930s, reporting standards began to improve. By the 1990s, with the digitization of financial records and the emergence of online trading platforms, investment statements evolved into detailed, standardized documents provided monthly or quarterly.

Today, these statements have become indispensable tools for both retail and institutional investors. They not only reflect the current value of one’s portfolio but also serve as a lens into investment performance, fees, and risk exposure.

Core Principles of Investment Statements

What Is an Investment Statement?

An investment statement is a periodic report—usually monthly or quarterly—provided by your brokerage or financial advisor. It summarizes the performance of your investments during the reporting period. It includes:

1. Account Summary – Shows the total value of your holdings.

2. Asset Breakdown – Lists each investment (stocks, bonds, ETFs, etc.) and their individual performance.

3. Transaction History – Details any buys, sells, dividends, or fees.

4. Performance Metrics – Offers insights such as total return, interest earned, and unrealized gains or losses.

5. Fees and Expenses – Discloses any management or transaction fees deducted during the period.

Understanding these sections is critical to managing your portfolio effectively and avoiding costly mistakes.

Why They Matter

Many investors overlook their statements, assuming everything is being managed correctly. However, this passive approach can lead to:

– Misaligned asset allocation

– Unexpected fees

– Undetected errors or unauthorized transactions

By reading and interpreting your statements regularly, you retain control over your financial future.

Real-World Examples

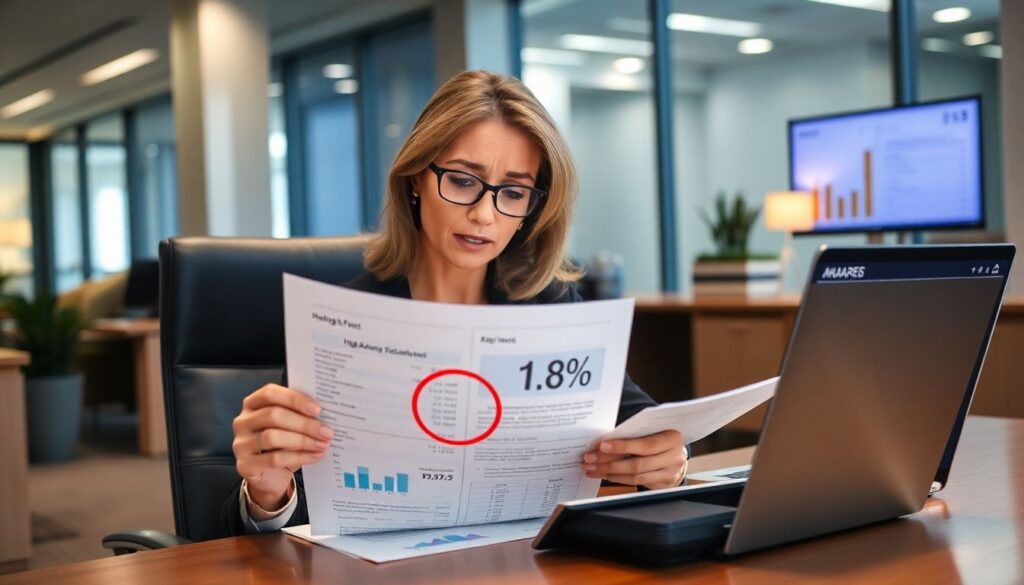

Case 1: Unnoticed Management Fees

In 2021, a mid-level executive named Karen noticed her retirement savings were growing slower than expected. After carefully reviewing her quarterly statement, she discovered a 1.8% annual advisory fee—much higher than the industry average of 0.5%-1.0%. Over 10 years, this would have cost her tens of thousands in lost compounding. She switched to a lower-cost advisor and reallocated her portfolio, ultimately improving her returns.

Case 2: Hidden Asset Concentration

A young investor, Marco, believed he had a diversified portfolio. However, after reviewing the ‘Asset Breakdown’ section of his statement, he realized that nearly 70% of his investments were in tech stocks. This concentration made his portfolio vulnerable to market corrections. After consulting an advisor, he diversified into healthcare, energy, and fixed income instruments, reducing his overall risk.

Case 3: Dividend Reinvestment Confusion

Sophia, a retiree, was surprised by a tax bill related to dividends. Her statement had clearly shown automatic dividend reinvestment, but she mistakenly thought that reinvested dividends were tax-free. Although reinvested, dividends are still considered taxable income. A tax advisor helped her adjust her strategy to minimize future liabilities.

Common Misconceptions

1. “If my account is growing, I don’t need to check the statement.”

Even if your portfolio is increasing in value, it may not be performing optimally. Growth could be due to a bull market rather than sound asset allocation or low fees. Regular review ensures that your investments align with your goals and risk profile.

2. “All fees are clearly visible.”

Not always. Some fees are embedded in fund performance or labeled in ways that aren’t immediately obvious. Words like ‘expense ratio’ or ‘load’ might seem benign but have a significant impact over time.

3. “I can’t understand it without a financial advisor.”

While advisors are helpful, investment statements are designed to be accessible. Key figures like account value, returns, and fees are typically marked in bold or summarized at the top. Taking the time to learn basic financial terminology can empower any investor.

4. “Performance numbers are always accurate.”

Statements may show returns that don’t account for inflation, taxes, or external deposits and withdrawals. It’s important to understand whether the reported performance is net of fees and how it compares to benchmarks like the S&P 500.

How to Analyze Your Investment Statement: A Step-by-Step Guide

1. Start with the Account Summary – Verify the total value and compare it with the previous period.

2. Review Asset Allocation – Ensure your investments are diversified across sectors and asset classes.

3. Check for Unusual Transactions – Look out for unauthorized trades or unexpected fees.

4. Compare Performance Against Benchmarks – If your mutual fund underperforms the market consistently, consider alternatives.

5. Review Dividends and Interest – Understand whether they’re being reinvested or distributed, and how that affects your taxes.

6. Scrutinize Fees – Ask questions if you see high advisory or management costs. Even small percentages add up over time.

Final Thoughts

Understanding your investment statements isn’t just for finance professionals—it’s a fundamental part of responsible investing. These documents hold essential clues about your financial health and future. With a bit of effort and periodic review, anyone can use them to make informed, strategic decisions.

By demystifying the jargon and focusing on key sections, you gain more than knowledge—you gain control. And in the world of investing, control is power.