Why Your Financial Plan Has To Survive Bad Markets, Not Just Good Ones

Most people start planning money goals assuming “normal” markets. Then the first big drop hits, panic kicks in, and the nice-looking spreadsheet gets ignored. financial planning for market downturns is less about predicting the next crash and more about building a plan that assumes bad years will come regularly. If you design everything around smooth growth, you’re basically building a house on sand. The goal is simple: when stocks fall, your lifestyle, your sleep, and your long‑term goals should wobble a bit, but not collapse. That means shifting from “How do I make the most?” to “How do I survive the worst and still end up where I want?”

Beginners often skip this mental shift. They chase “high return” stories, forget that risk can show up at the worst time, and then sell at the bottom. Let’s fix that by building a plan that’s prepared for ugly markets from day one.

Common Rookie Mistake: Confusing a Bull Market With Skill

A classic beginner error is assuming that a few good years mean they’re naturally great investors. Markets rise more often than they fall, so it’s easy to believe you’ve “figured it out” when everything is up. Then a sharp drop comes, and suddenly that aggressive, concentrated portfolio doesn’t feel so smart. New investors usually don’t have a written plan, just a vague idea: “I’ll invest in what’s hot and sell when it looks bad.” That’s not a plan; that’s improvisation under stress. When prices drop 20–30%, emotions take over, and those improvised decisions are usually wrong.

The antidote: build clear rules before trouble starts. Decide in advance how much you’ll invest in stocks, how much in safer assets, how long your money can stay invested, and what will trigger a change.

Step One: Start With Cash Flow, Not Charts

Before worrying about how to protect investments during a market crash, you need a boring but essential base: a solid cash flow plan. Crashes hurt most when you’re forced to sell investments at low prices just to pay bills. So the first layer of a crisis‑proof plan is knowing exactly what comes in, what goes out, and what you can cut if needed. Long, complicated budgets are nice, but you really need three numbers: required expenses, flexible expenses, and regular savings. Once you see those clearly, you can shape an emergency buffer that covers essentials even if your income drops, so market chaos doesn’t instantly become life chaos.

Newbies often skip this and jump straight to “Which fund should I buy?” Then they’re surprised when a job loss plus a market downturn forces them to sell their long‑term investments at the worst moment. Don’t give the market that kind of power over your life.

The Emergency Fund: Your First Line of Defense

Think of an emergency fund as your personal “shock absorber.” Its job is not to earn high returns; it’s to buy you time. During recessions, time is priceless.

A practical approach:

– Aim for 3–6 months of essential expenses in cash or a very liquid account

– If you’re self‑employed or in a cyclical industry, increase that to 6–12 months

– Keep this money separate from your investment accounts

Beginners often make two big mistakes here. First, they treat the emergency fund as an “extra investment” and chase yield, locking it into risky or illiquid products. Second, they underestimate how fast costs add up when income drops. A dedicated, boring cash buffer lets you stay invested when others are forced to panic‑sell.

Risk Level: Matching Your Portfolio to Real Life, Not Your Ego

The next pillar is risk. Most people say they’re “okay with risk” when markets are up. The real test is your behavior during a 30–40% drop. Do you stay invested, rebalance, or sell everything? Your financial plan has to reflect your actual tolerance, not the bravado you feel after reading a few optimistic forecasts. This is where portfolio diversification services for risk management can be genuinely useful: they help spread your money across different asset classes, regions, and sectors so that no single event can wreck your entire future. The idea is not to kill risk but to avoid being exposed to one fatal risk at the wrong time.

New investors often load up on one sector, one country, or even one company, convinced they “really understand it.” That’s not insight; that’s concentration risk, and downturns love to punish it.

Smart Diversification: Not Just Owning “A Lot of Stuff”

True diversification is more than having many ticker symbols. You want assets that don’t always move in the same direction at the same time. That usually means a mix of:

– Stocks (broad, low‑cost index funds rather than a few “favorite” companies)

– Bonds or bond funds with different maturities

– Some cash or cash‑like instruments

– Possibly real assets (like REITs) if they fit your risk level

A beginner mistake is buying a bunch of tech funds and calling it diversified. That’s just one theme repeated. Another mistake is constantly tinkering. Diversification works over years, not weeks. Your job is to set a reasonable mix, then rebalance occasionally, not reinvent your allocation every headline cycle.

Guardrails for Big Drops: What You’ll Do Before, During, and After

When planning how to protect investments during a market crash, think in terms of guardrails, not precise predictions. You can’t know when the next crash hits, but you can script your behavior. Before a crash, you set your asset allocation, savings rate, and emergency fund. During a crash, you follow pre‑written rules: no panic selling, no big strategy changes within 72 hours of scary news, and rebalancing only at set intervals. After a crash, you review but don’t rewrite your whole philosophy just because one event hurt.

New investors often do the opposite. They improvise during the storm, follow social media tips, and confuse activity with control. A simple, written “if X happens, I will do Y” note can save you from your own fear when screens turn red.

Retirement Planning in a World That Never Stays Calm

Retirement planning strategies for volatile markets need to assume sequence risk: the danger that bad returns come early in retirement, when you’re starting to withdraw. Two people with the same average return can end up in very different places if one hits a major downturn in the first years of retirement. Mitigating this means entering retirement with enough safe assets to cover several years of withdrawals, using flexible spending rules, and possibly having a “floor” of guaranteed income from pensions or annuities. The idea is that a few bad years won’t force you to slash your lifestyle permanently or go back to work unwillingly.

Beginners planning retirement often look only at average return projections and ignore timing. Markets don’t care about your birthday; your plan has to respect that.

When and How to Use Professional Help

Not everyone needs an advisor, but a good one can be a buffer between you and your worst impulses. The best financial advisors for recession planning don’t just pick funds; they help design rules, stress‑test your plan against ugly scenarios, and talk you out of panic moves. If you work with a pro, ask how they handled 2008, 2020, or other major downturns, and what their clients actually did during those periods. You’re not just buying technical knowledge; you’re buying emotional discipline.

A novice error is hiring someone solely because they promised higher returns or showed glossy back‑tests. During real downturns, you want a guide who focuses on survival, not on beating a benchmark every quarter.

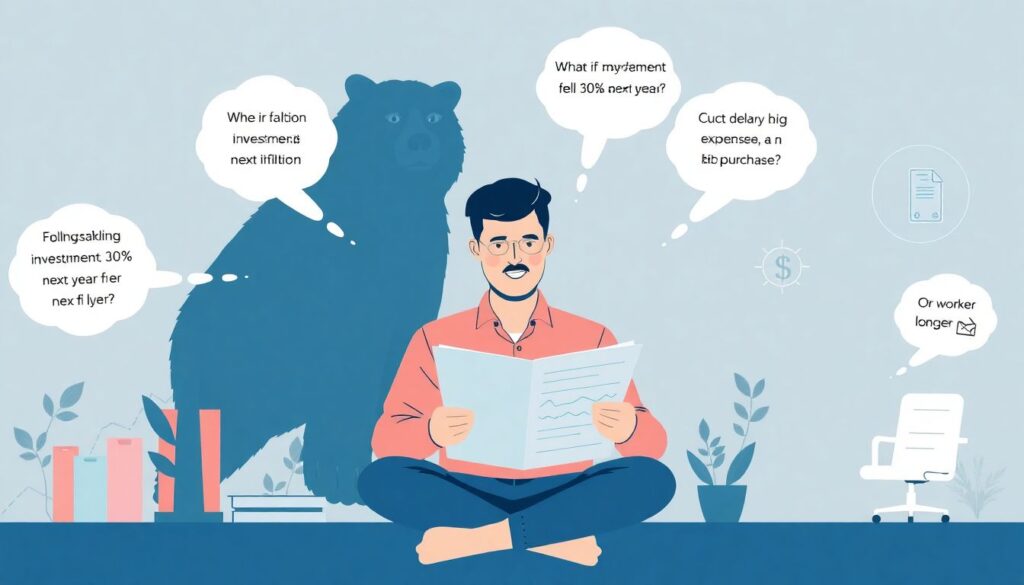

Stress‑Testing Your Plan: Practice the Worst Case Before It Happens

A resilient plan isn’t based on hopeful scenarios. Run your numbers assuming: lower returns, temporary job loss, higher inflation, and at least one deep bear market. Ask: “If my investments fell 30% next year, what would I actually do?” Would you cut expenses? Delay a big purchase? Work longer? Adjust retirement withdrawals? Stress‑testing forces you to confront trade‑offs now, when you’re calm, rather than invent them in a panic.

Many beginners skip this because it feels negative. But pretending downturns won’t happen doesn’t make you optimistic; it makes you fragile. Strong plans are built by people who accept that bad years are part of the journey and design around them.

Putting It All Together So You Don’t Have to Start Over After Every Crash

To build a financial plan that endures market downturns, stack the basics in order: stable cash flow, a real emergency fund, honest risk assessment, thoughtful diversification, clear rules for crises, and long‑term retirement planning that assumes volatility, not calm. Along the way, avoid rookie mistakes: overconfidence in good times, concentration in one idea, chasing yield with safety money, and improvising under stress.

Your goal isn’t to avoid every loss; that’s impossible. The real win is staying invested, staying solvent, and staying sane through multiple market cycles. If your plan lets you do that, you’re already far ahead of most investors—no matter what the headlines say.