Why Building a Safe Future on a Fixed Income Matters More Than Ever

Keeping money steady is tough when prices jump around and your paycheck has stopped. According to the U.S. Bureau of Labor Statistics, prices rose over 17–19% between 2020 and 2024, while Social Security cost-of-living adjustments only loosely chased that. That gap is exactly what eats into a “fixed” income and turns a comfortable budget into a tight one over just a few years.

At the same time, populations are aging fast. The OECD expects the share of people over 65 in developed countries to grow from about 17% in 2020 to more than 26% by 2050. That means more people depending on pensions, annuities, and savings, and fewer workers paying into the system. For you personally, this translates into one clear message: relying only on government benefits is risky, so you need your own plan for stability.

Step 1: Get Completely Clear on Your Real Numbers

Track Every Dollar Without Making Yourself Miserable

You can’t build a financially safe future on a fixed income if you don’t know exactly what’s coming in and what’s going out. The goal isn’t to become an accountant; it’s to stop being surprised by your own bank statement.

Spend 30–60 days tracking everything: rent or mortgage, utilities, groceries, subscriptions, gifts, healthcare, “little treats,” and one-offs like car repairs. Use a notebook, a simple spreadsheet, or a basic app. The tool doesn’t matter; consistency does.

Then do one quick pass: mark each expense as “must-have,” “nice-to-have,” or “why-did-I-buy-this.” You’ll usually find 5–15% of your spending that’s not really improving your life. That’s your first safety margin.

Build a Simple Fixed-Income Budget That Survives Inflation

Once you see the numbers, design a budget that assumes costs will creep up over time. A practical trick: each year, try to shave 1–2% off discretionary spending (eating out, entertainment, subscriptions) and redirect that toward savings or debt payoff. That’s how you build “give” into a tight budget.

If you’re struggling with credit cards, personal loans, or medical bills, look for fixed income budgeting and debt consolidation help before things snowball. Nonprofit credit counseling agencies can often roll multiple payments into one predictable monthly bill at a lower rate, which is exactly what you want when your income doesn’t move much.

Step 2: Build a Realistic Safety Net

Emergency Fund, Even on a Tight Income

Yes, you still need an emergency fund on a fixed income. No, it doesn’t have to be the textbook “six months of expenses” right away. Start with a micro-goal: one month of essential bills in a separate savings account at your bank or credit union.

Add to it automatically: $25, $50, or $100 a month, whatever fits. The automation matters more than the amount. Over a few years, that small drip can grow into a serious cushion that keeps a broken fridge or car repair from turning into credit-card debt.

Match Your Cash Reserves to Market Risk

Here’s a simple rule of thumb that many fixed-income retirees ignore until a crash happens: keep 1–3 years of basic living expenses in very low-risk, highly liquid places—high-yield savings, money market funds, or short-term CDs.

That buffer means if markets drop, you can live off your cash reserves for a while instead of selling investments at a loss. It’s a boring strategy. Boring is what protects you.

Step 3: Learn How to Invest on a Fixed Income for Retirement

Why “No Risk” Usually Means “Hidden Risk”

A lot of people on fixed incomes gravitate to whatever sounds “guaranteed.” The problem is that if your savings sit only in low-interest accounts while inflation runs at 3–4%, your money quietly shrinks in purchasing power every year.

So when you think about how to invest on a fixed income for retirement, you’re really trying to balance two enemies: market volatility and inflation. Too much market risk, and a downturn can hurt your income. Too much “safety,” and inflation slowly erodes your standard of living.

Practical Portfolio Ideas for Fixed-Income Households

You don’t need to become a stock picker. You do need a sensible mix of assets that can outpace inflation without swinging wildly. Very broadly, that might look like:

1. Cash & short-term reserves

High-yield savings, money market funds, or short-term CDs for 1–3 years of expenses.

2. Bonds and bond funds

Government bonds, investment-grade corporate bonds, or bond ETFs to provide steady income and lower volatility than stocks.

3. Dividend-paying stock funds

Broad index funds or ETFs with solid, diversified companies that pay regular dividends, giving you growth plus income.

4. Optional annuities (with caution)

Certain low-cost, plain-vanilla annuities can turn part of your savings into a lifelong monthly paycheck, shifting longevity risk to an insurance company.

The exact percentages should match your age, risk tolerance, and other income sources. That’s where professional help can be worth its fee.

Step 4: Choosing Advice You Can Actually Trust

When Professional Help Makes Sense

If all of this feels like a second job, you’re not alone. The industry has noticed this pain point, which is why fixed income retirement planning services have grown quickly in the last decade. Demographics are driving this: millions of retirees with pensions, Social Security, and modest savings are looking for tailored guidance, not one-size-fits-all investing.

Look for someone who acts as the best financial advisor for fixed income retirees in practice, not just in marketing. That usually means:

– Working as a fiduciary (legally required to put your interests first)

– Fee-only or transparent fee-based, not paid mainly by commissions

– Experience with retirement income planning, taxes, and Social Security strategies

– Comfortable explaining things in plain language, not jargon

Red Flags to Watch For

If an advisor pushes a single product as the magic answer, especially a complex annuity or high-fee mutual fund, pause. Ask: “How are you paid on this?” If the answer is vague or defensive, that’s your sign to walk away.

Step 5: Smart Debt and Cash-Flow Management

Don’t Let Old Debts Eat Your Future

Entering retirement with high-interest debt is like running a marathon with a backpack full of rocks. Each payment reduces the cash you can use for healthcare, food, or even small pleasures that make retirement enjoyable.

If you’re still working part-time or fully employed, prioritize paying down the highest-interest debt first while you have more income flexibility. Think of every dollar of interest you avoid as guaranteed “earnings.”

Using Consolidation and Negotiation Wisely

Fixed income budgeting and debt consolidation help can simplify your life: one payment, one date, and often a lower interest rate. Just be careful not to stretch the loan so long that you pay more interest over time.

In many cases, you can also call creditors—especially medical providers—and negotiate payment plans or discounts. They would rather get something consistent than chase you for overdue bills.

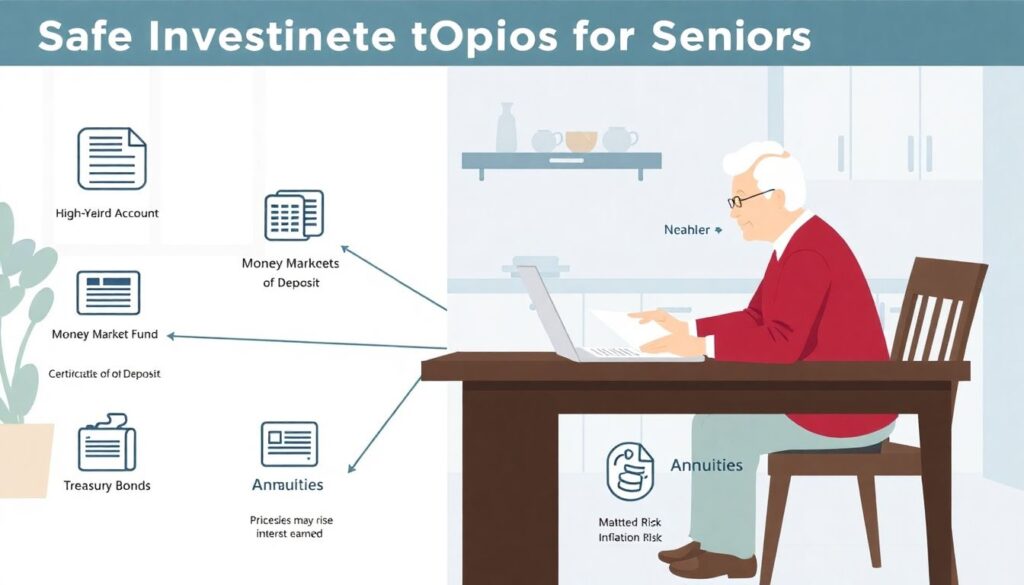

Step 6: Safe Investment Options for Seniors on Fixed Income

What “Safe” Actually Means Today

Safe investment options for seniors on fixed income aren’t truly “risk-free”; they just carry different types of risk. Here are some commonly used tools and the main thing to watch with each:

– High-yield savings and money market funds – Great for short-term needs; main risk is inflation outpacing interest.

– Certificates of Deposit (CDs) – FDIC-insured if under limits; risk is locking money up at a low rate while inflation or rates climb.

– Treasury bonds and TIPS – Backed by the government; TIPS adjust for inflation but can be sensitive to interest-rate changes.

– Stable value funds (often in 401(k)s) – Aim for steady returns with low volatility; check fees and underlying investments.

The economic backdrop matters here. With interest rates higher than they were in the 2010s, conservative assets finally pay something again, which is good news for fixed-income retirees. But it also means bond prices can fluctuate more when rates move, so diversification inside even the “safe” bucket is wise.

Combining Safety with Flexibility

Instead of chasing the “best” single product, think in layers: quick-access money for emergencies, medium-term money in CDs or bonds, and longer-term growth in diversified funds. That layered approach is what keeps your plan standing when the economy shifts.

Step 7: Plan for the Long Game – Health, Inflation, and Longevity

Healthcare: The Often-Ignored Budget Buster

Healthcare is one of the fastest-growing expenses for retirees. Studies from Fidelity and others estimate that an average 65-year-old couple in the U.S. may need several hundred thousand dollars over their remaining lifetimes for medical costs, including premiums and out-of-pocket spending.

That number is scary, but the practical takeaway is simple:

– Compare Medicare plans annually instead of letting them auto-renew.

– Use Health Savings Accounts (HSAs) if you’re still eligible and working.

– Factor dental, vision, and hearing costs into your budget instead of treating them as surprises.

Thinking Like an Economist About Your Own Life

On a bigger scale, aging populations are reshaping entire industries—healthcare, pharmaceuticals, home care, retirement housing, and financial services. Companies are building products and apps designed just for retirees living on fixed incomes, from medication-discount programs to robo-advisors that automate withdrawals.

For you, this shift is both a warning and an opportunity. Government systems may come under strain as more retirees draw benefits, but private markets are competing hard to serve you better. If you stay informed and willing to switch providers when it makes sense—insurance, banks, advisors—you can often improve your financial safety without increasing your income.

Pulling It All Together into a Practical Plan

A Simple Action Roadmap

You don’t need to do everything at once. Over the next 12 months, aim for:

1. Month 1–2: Track all income and expenses; build a realistic fixed-income budget.

2. Month 3–4: Start or strengthen your emergency fund; set up automatic transfers.

3. Month 5–6: Review all debts; pursue consolidation or renegotiation where helpful.

4. Month 7–9: Set up or adjust your investment mix to balance safety and inflation protection.

5. Month 10–12: Interview at least two advisors or planners who specialize in retirement income and choose the one that suits your needs.

Each small step tightens the net under you. Over a few years, that turns into something powerful: stability, predictability, and fewer sleepless nights.

You can’t control inflation, markets, or policy changes. You can control your information, your habits, and your use of the tools and services now built specifically for people living on fixed incomes. That’s how you build a financially safe future that holds up under real-life pressure.