Understanding Your Risk Profile: The Foundation of Smart Investing

Before you can build a strong investment plan, you need to understand your unique risk profile. This is more than just asking yourself if you’re a “conservative” or “aggressive” investor. Your risk profile combines your financial goals, investment horizon, income stability, and emotional tolerance for market volatility.

For example, a 30-year-old software engineer with a stable job and no dependents may be more comfortable with a higher level of risk than a 60-year-old nearing retirement. In practice, this means the younger investor could allocate a higher percentage of their portfolio to equities, while the older investor might lean toward fixed-income securities and cash equivalents.

Key Factors That Define Your Risk Profile

To accurately assess your risk profile, consider these core elements:

– Time Horizon: How long can you leave your money invested? Longer horizons often allow for more risk.

– Financial Goals: Are you saving for retirement, a home, or your child’s education? Each goal may require a separate strategy.

– Risk Tolerance: How do you react during market downturns? Would a 20% portfolio drop keep you up at night?

Tools like the Vanguard Investor Questionnaire or the Morningstar Risk Profiler can help you quantify your risk tolerance. But numbers alone aren’t enough—honest self-reflection is crucial. In 2020, during the COVID-19 crash, many investors discovered their true tolerance only after watching their portfolios drop by double digits.

Aligning Investment Strategy with Risk Appetite

Once you’ve identified your risk profile, the next step is to align your investment strategy accordingly. This means choosing asset classes and allocation ratios that reflect your comfort level and financial targets.

Asset Allocation: The Core of Portfolio Planning

Asset allocation is the distribution of your investments across major asset classes—typically stocks, bonds, and cash. It’s the single most important factor influencing long-term performance and volatility.

Here’s a practical breakdown:

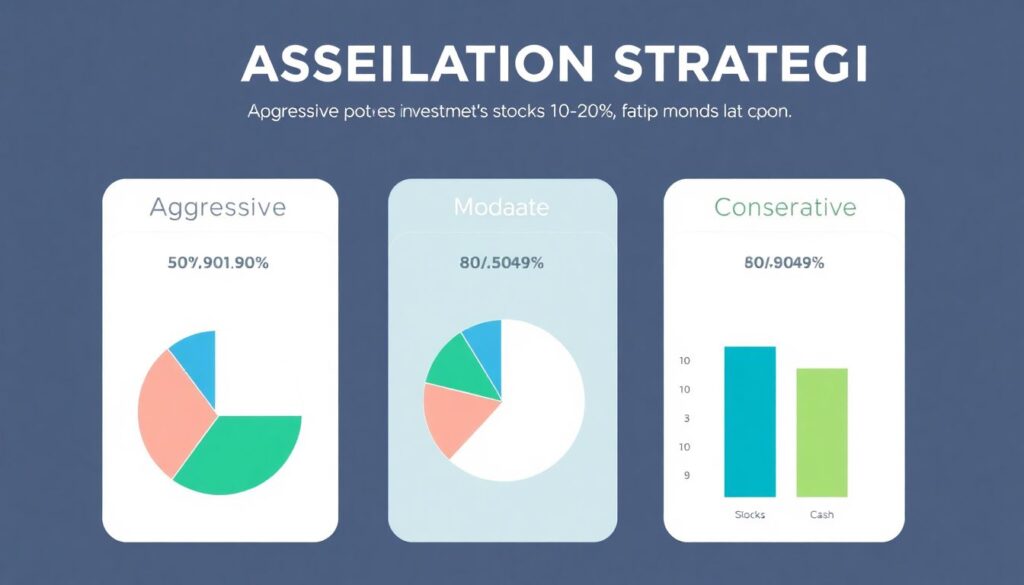

– Aggressive Profile: 80–90% stocks, 10–20% bonds and cash

– Moderate Profile: 60% stocks, 30% bonds, 10% cash

– Conservative Profile: 30–40% stocks, 50–60% bonds, 10–20% cash

A 35-year-old with a high-risk tolerance might adopt an 85/15 stock-to-bond ratio, focusing on growth-oriented ETFs like the Vanguard Total Stock Market ETF (VTI) and emerging markets exposure. In contrast, a risk-averse retiree may prefer a 40/60 mix, emphasizing municipal bonds and dividend-paying blue-chip stocks.

Diversification: Spreading Risk Effectively

Diversification doesn’t just mean owning different stocks. It means spreading your investments across asset classes, sectors, and geographies to reduce exposure to any single risk.

Consider these diversification strategies:

– Geographic Diversification: Combine U.S., European, and Asian equities to reduce regional risk.

– Sector Diversification: Avoid overconcentration in tech or energy; use sector ETFs to balance exposure.

– Instrument Diversification: Mix individual stocks, mutual funds, ETFs, and REITs for broader coverage.

A real-world example: During the 2008 financial crisis, portfolios heavily weighted in U.S. financials lost up to 50%, while those diversified into international consumer staples and healthcare saw less than half that loss.

Rebalancing and Adjusting Over Time

Your risk profile isn’t static. Life events—marriage, job changes, children, or nearing retirement—can shift your risk appetite. That’s why periodic rebalancing is essential.

When and How to Rebalance

Rebalancing involves realigning your portfolio to maintain your target asset allocation. For instance, if your 70/30 stock-bond mix drifts to 80/20 due to a bull market, you’d sell some stocks and buy bonds to restore balance.

You can rebalance:

– Annually: A good rule of thumb for most investors

– Threshold-based: When an asset class deviates by more than 5–10%

– Life-event driven: Adjust after significant personal or financial changes

Many robo-advisors like Betterment or Wealthfront offer automatic rebalancing, which is ideal for hands-off investors. If managing manually, set a calendar reminder to review your portfolio every 6 or 12 months.

Putting It All Together: A Practical Example

Let’s take Sofia, a 40-year-old marketing executive aiming to retire at 65. With moderate risk tolerance and a 25-year horizon, she builds a portfolio of:

– 60% stocks (40% U.S., 20% international)

– 30% bonds (mix of corporate and government)

– 10% cash and short-term instruments

She reviews her portfolio every January and rebalances if any asset class shifts more than 5%. In 2022, when tech stocks underperformed, her international exposure helped cushion the blow, validating her diversified approach.

Final Thoughts: Stay Disciplined and Adaptable

Creating an investment plan that matches your risk profile isn’t a one-time task—it’s an ongoing process. The key is to remain disciplined during market swings and flexible when your life circumstances change. By aligning your strategy with your true risk tolerance, you’ll not only protect your capital but also sleep better at night—knowing your investments are working in harmony with your goals.